Annuity Company Issuer Review: Pacific Life

Since this investment is usually for the long term such as 10 years, it is important that the annuity company itself is financially sound. The guarantees in the annuity are back by the insurance company and not from a government agency. However each state’s Guaranty Association has a dollar amount, usually $100,000, that it will refund if an annuity carrier went bankrupt. Think of it as a second layer of protection.

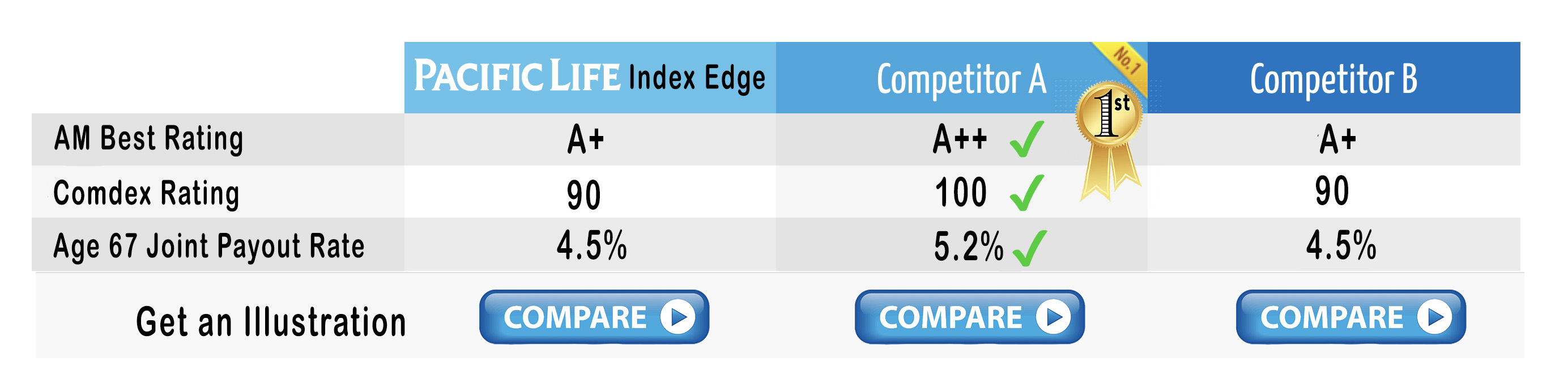

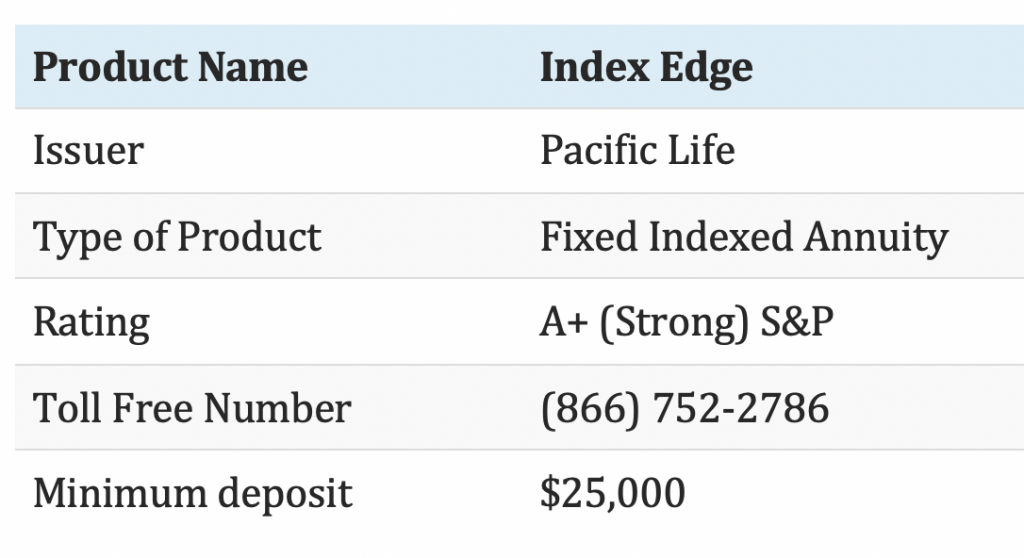

![]() Based in Newport Beach,California, Pacific Mutual Life was founded in 1868 by former California Governor Leland Stanford who also founded Stanford University in Palo Alto, CA. Stanford also was the first policy holder of the company. After Stanford died and his university (Stanford University) was strapped for money, his wife used the money from the policy to pay for professors. Pacific Life is a mutual company, meaning it is not listed on a stock exchange, thought of being superior company makeup is rated “A+” (Superior) by A. M. Best Company (as of March 20, 2015) and has a Comdex Rating of 90 (out of possible 100) as of 04/2018. It has over $150 Billion in assets and is a Fortune 500 company.

Based in Newport Beach,California, Pacific Mutual Life was founded in 1868 by former California Governor Leland Stanford who also founded Stanford University in Palo Alto, CA. Stanford also was the first policy holder of the company. After Stanford died and his university (Stanford University) was strapped for money, his wife used the money from the policy to pay for professors. Pacific Life is a mutual company, meaning it is not listed on a stock exchange, thought of being superior company makeup is rated “A+” (Superior) by A. M. Best Company (as of March 20, 2015) and has a Comdex Rating of 90 (out of possible 100) as of 04/2018. It has over $150 Billion in assets and is a Fortune 500 company.

Surrender Fees:

Surrender charges/fees and periods for this annuity are the typical of most indexed annuities. Most fixed index annuities will have a 5 year, 7 year, 10 year, and 14 year surrender variation to choose from. Typically an annuity with a number in the product name with also most likely dictate the surrender period. Taking the longer surrender period will most likely give you a larger cap on indexes and a larger fixed rate option for index crediting. Typically fixed index annuities allow you to withdraw 10% of your accumulation value after the first year without surrender fees. However if you are under age 59 and a half, you are subject to a 10% IRS tax penalty as well as income taxes applied to the withdrawal.

Pacific Life Index Edge has the surrender charge option as seen above which coordinate with the duration of the annuity. Pacific Life Index Edge also has a 5 year, 7 year, and 10 year surrender charge annuities to choose from. You can also take out ten percent of your value starting in year 1 without a 10% penalty each year. If you are under age 59 1/2 there is a 10% IRS tax penalty on any dollars taken out.

Earning Interest:

Indexed annuities do a lot of things to confuse investors. Too many moving parts when it should be a simple two part calculation. The two parts are index crediting and income crediting. See most index annuities have two values that are tracked each year. The accumulation value account or (walk away money) and income value account (Lifetime income calculation value).

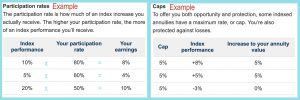

The accumulation value account will be based on your chosen crediting method based on an index. Examples are Annual point-to-point or Participation rates. Each year this is calculated and showed on your annual annuity statement under names like annuity value or accumulation values.

The accumulation value account will be based on your chosen crediting method based on an index. Examples are Annual point-to-point or Participation rates. Each year this is calculated and showed on your annual annuity statement under names like annuity value or accumulation values.

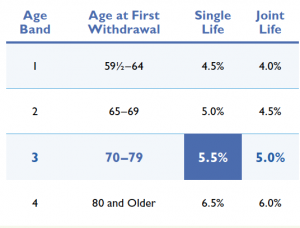

The income value is usually calculated on some “bonus” or “roll up rate” each year with a maximum of ten years. This roll up rate can be simple interest or compound interest. Simple interest would be the same calculate interest every year ( 5% simple interest for 4 years at $100,000 deposit would equal $5,000 credit each year for 4 years). Compound interest would be calculated as follows ( 5% compound interest at $100,000 deposit would equal $5,000 credit first year, $5,250 year 2, and $5,512 year 3). Then the income value is multiplied by an age range percentage band to calculate your guaranteed lifetime income payment. Income values can also be called protected payment base or protected income value.

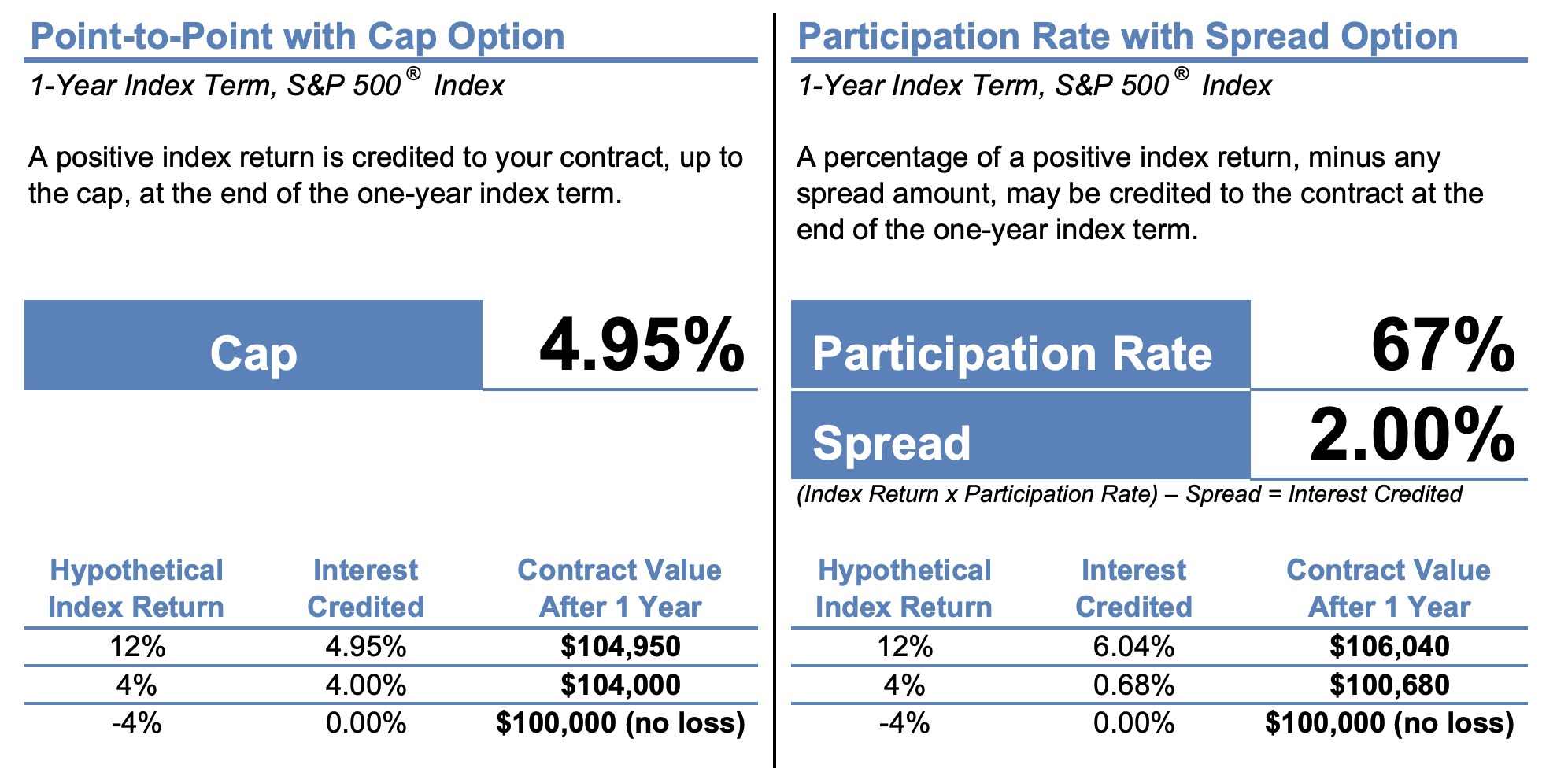

Pacific Index Edge offers a variety of Interest-Crediting Options.

- S&P 500® Index: 1-Year Point-to-Point with Cap

- S&P 500® Index: 1-Year Participation Rate with Spread

- S&P 500® Index: 5-Year Participation Rate with Spread

- BlackRock® EnduraTM Index: 2-Year Point-to-Point with Spread

- Fixed Account Option

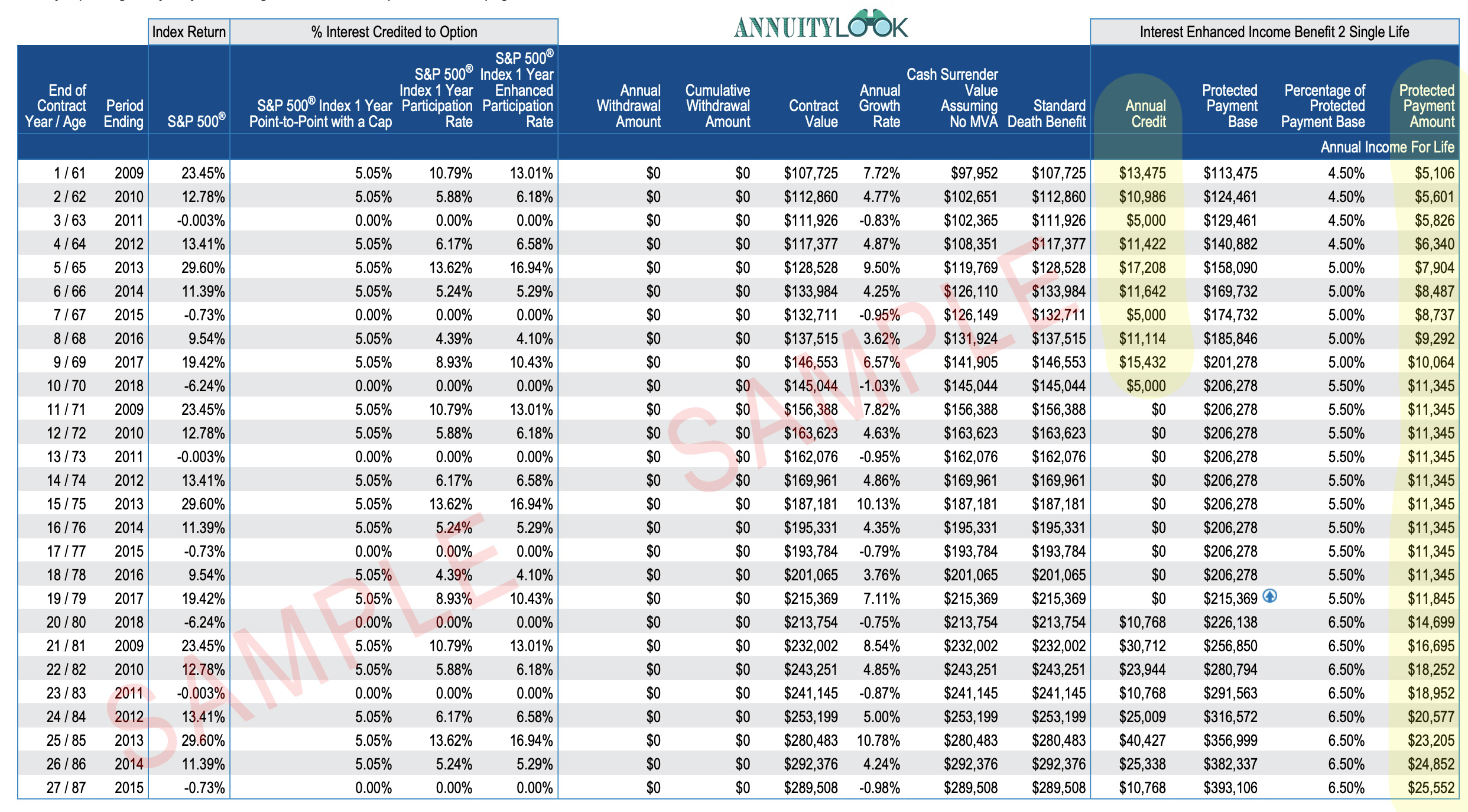

This is a sample Pacific Life Index Edge Illustration for a sixty year old male with getting “past historic” returns for their aggressive equity indexes.  You can see the interest earned every year on the Income Edge annuity in the fourth column from the right. This will give the Protected Payment Base, third column from right, a certain guaranteed annual income. The Protected Payment Amount , first column on the right hand side, is a calculation of the two factors the Protected Payment Base times the Percentage of Protected Payment Base column. This multiplication gives you annual income of $11,345 each year at the age of 70 in this example illustration. Ask your agent for the 0% index credit option to show you what the income will be to compare to the highly credited run agent illustration. See if any other index annuities from different companies will beat that income amount. If you want to see if there are other annuities that can go up against the Pacific Life Index Edge annuity, contact us via the Free Annuity Help form.

You can see the interest earned every year on the Income Edge annuity in the fourth column from the right. This will give the Protected Payment Base, third column from right, a certain guaranteed annual income. The Protected Payment Amount , first column on the right hand side, is a calculation of the two factors the Protected Payment Base times the Percentage of Protected Payment Base column. This multiplication gives you annual income of $11,345 each year at the age of 70 in this example illustration. Ask your agent for the 0% index credit option to show you what the income will be to compare to the highly credited run agent illustration. See if any other index annuities from different companies will beat that income amount. If you want to see if there are other annuities that can go up against the Pacific Life Index Edge annuity, contact us via the Free Annuity Help form.