What Will We Cover in this Annuity Review?

In this annuity review, we will be going over annuity details regarding the Jackson Perspective II annuity.

Investment type

Rates

Optional Benefits and Riders

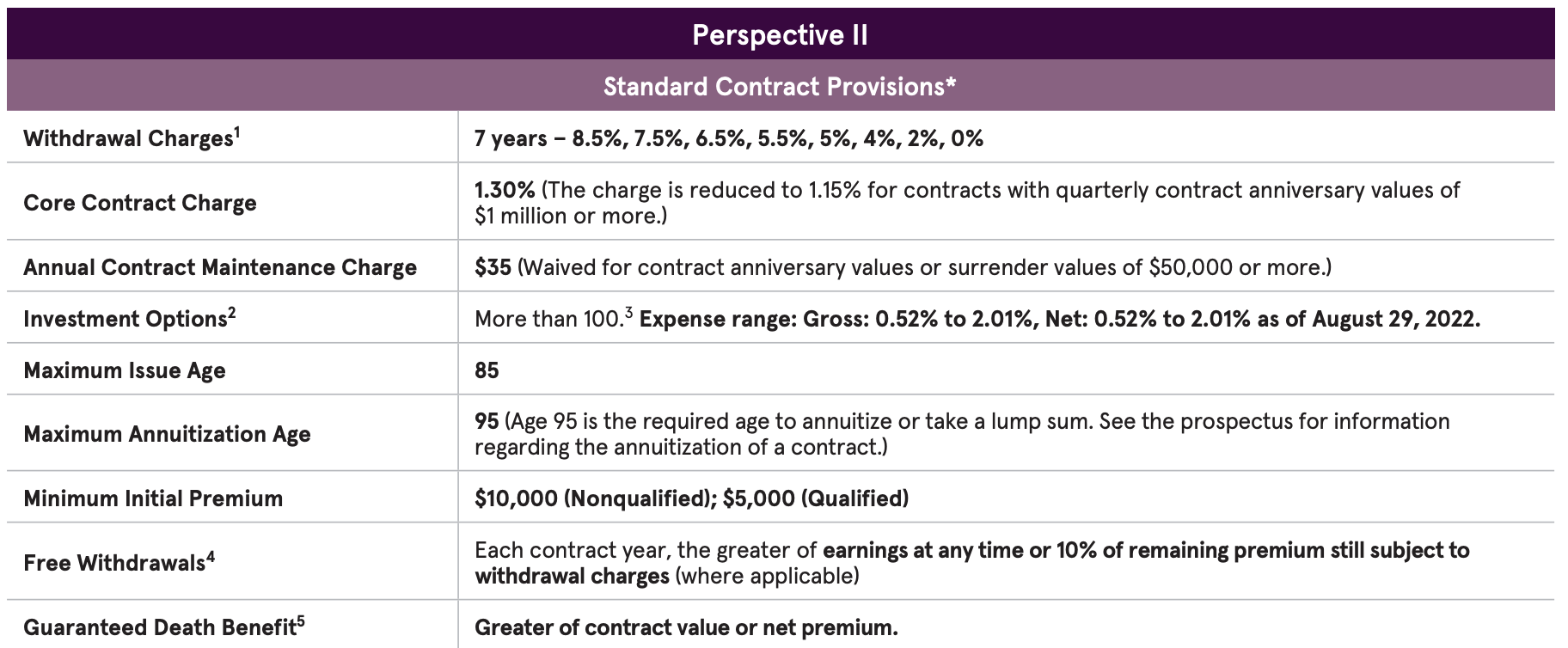

Fees

Return expectations

How it is used- Pros and Cons

In 2021, total annuity sales in the United States reached a record high of $69 billion. This is 40% more than last year and it represents one of many strategies that can protect retirees against market volatility while securing lifetime income for them as well!

When shopping for annuities, it’s important to be aware that each product may have a different focus. For example one product could provide death benefit protection or income while another provides growth-oriented security – with both having the same name but differing features and rider options attached!

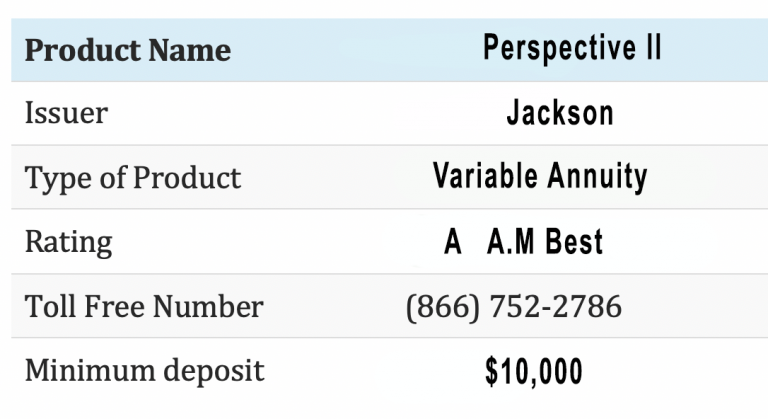

Annuity Company Issuer Review: Jackson

Jackson annuities is a private financial institution founded in 1961. Jackson specializes in retirement annuities and has $298 billion in total assets making it the 7th largest US life insurance company ranked by total statutory assets. Jackson has an A (Excellent) A.M. Best financial strength rating, the third highest of 13 rating categories. Jackson was also ranked as the #1 seller of annuities and the #1 seller of variable annuities in the US during 2021. The Jackson Perspective II is one of the most popular products offered by Jackson Annuities, and it has consistently received high marks.

Since this investment is usually for the long term such as 10 years, it is important that the annuity company itself is financially sound. The guarantees in the annuity are back by the insurance company and not from a government agency. However each state’s Guaranty Association has a dollar amount, usually $100,000, that it will refund if an annuity carrier went bankrupt. Think of it as a second layer of protection.

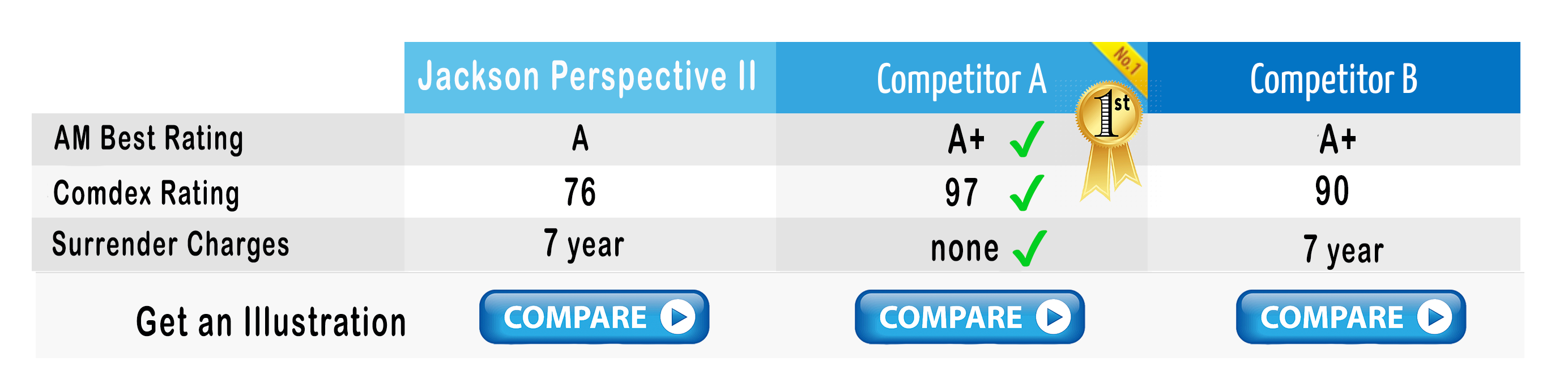

Comparison:

Table below will update as the competition changes. Currently, there are some great choices for retirement annuities. To request a side by side, click on the compare button below, and our Retirement Income Certified Professional® will be happy to answer any question you might have (Click Here).

Income features?

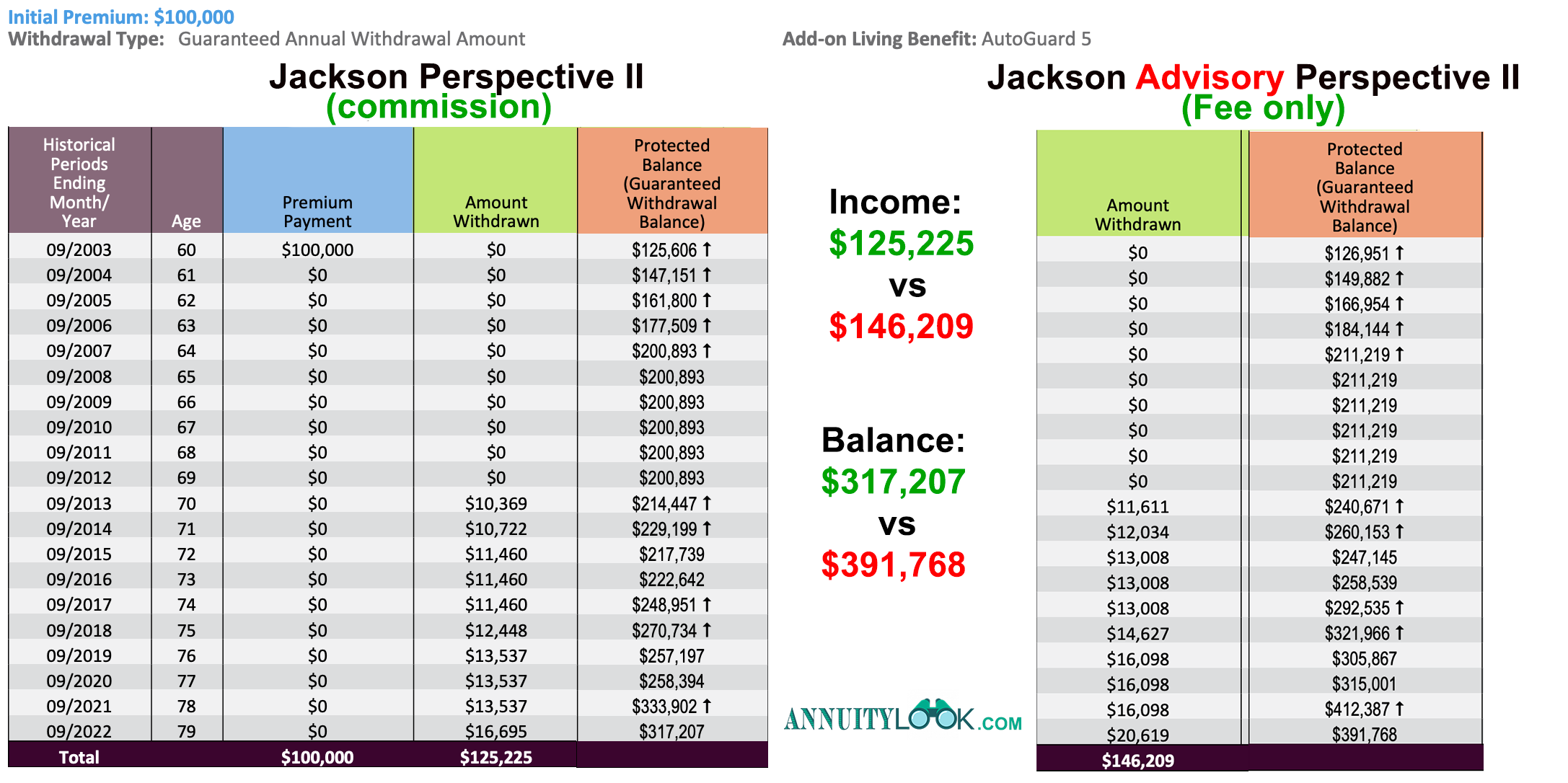

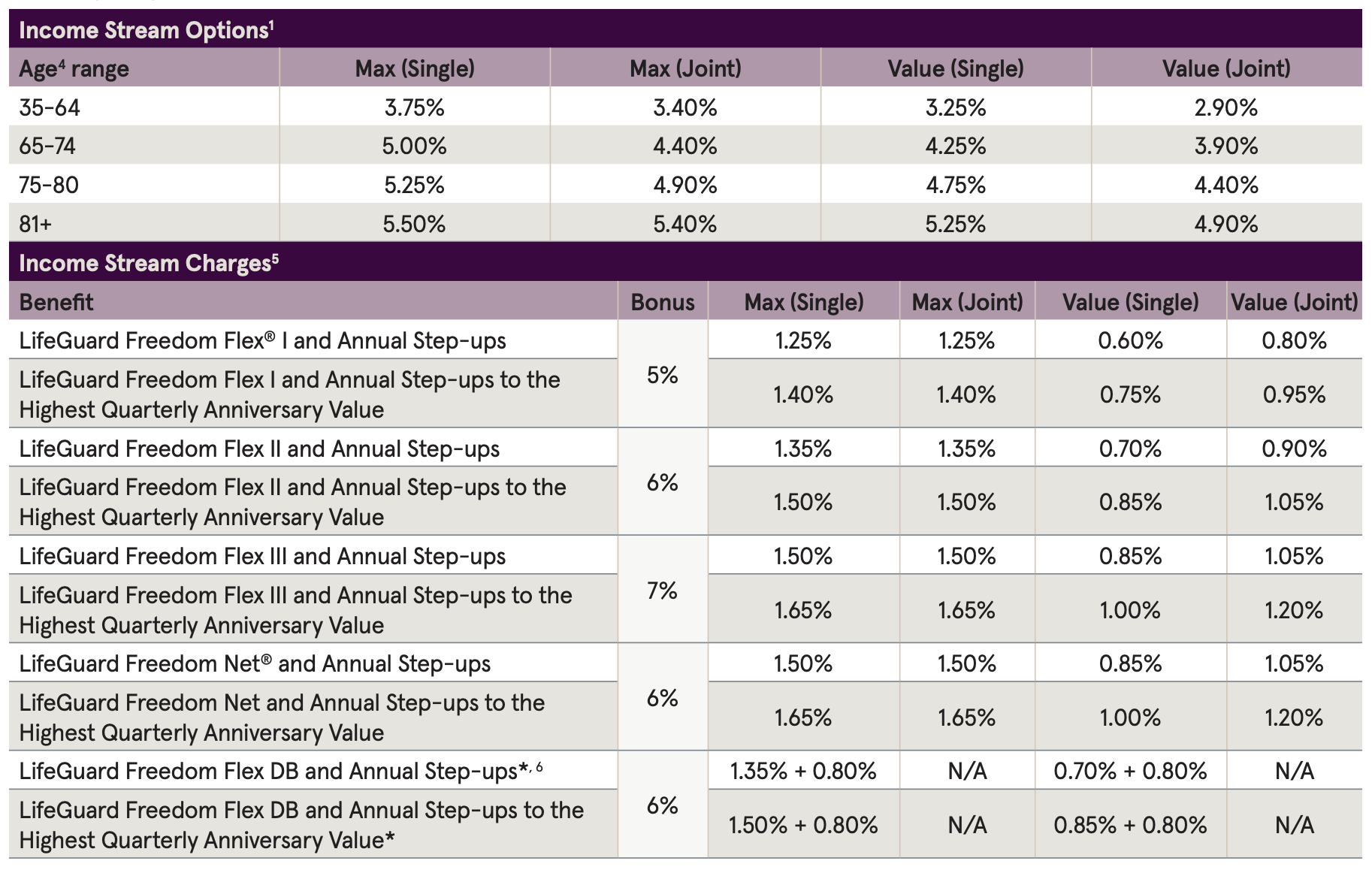

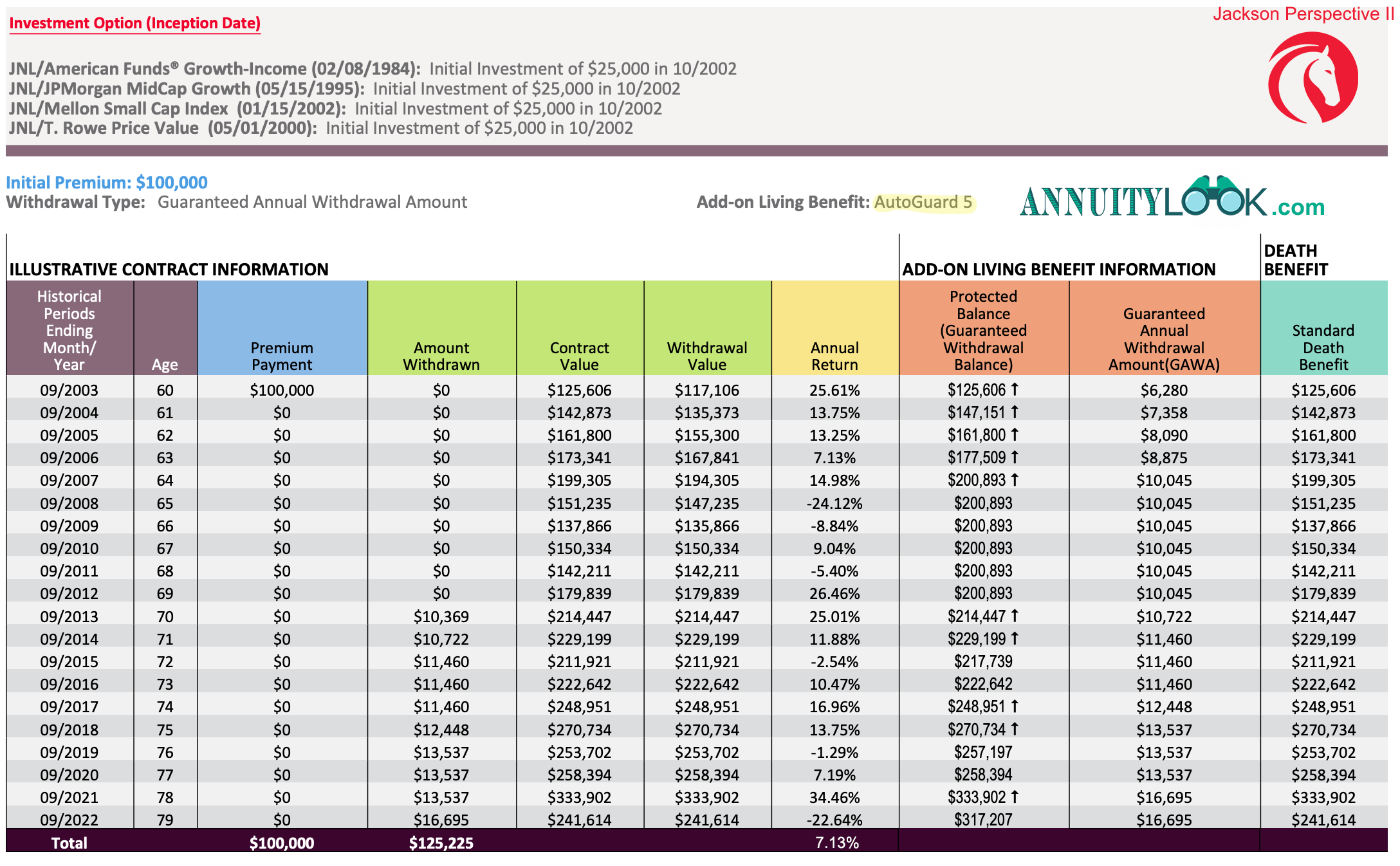

The nice feature of the Jackson Perspective II annuity is that it has over ten different optional income riders for lifetime income. Typical income rider fees can be as high as 2% per year charge on the accumulation value of the annuity. An Income Stream, elected with any of the LifeGuard Freedom® suite of living benefits for an additional charge, provides you flexible and cost-conscious withdrawal options. This allows you to select a specific Income Stream for your unique retirement needs. Some of the advisor’s favorite income rider options are the AutoGuard 5 income rider return of premium feature (0.85% annual cost) and the LifeGuard Freedom Flex II with Annual Step-ups and 6% bonus (1.35% annual cost). AutoGuard 5 is a income rider (GMWB) guaranteed minimum withdrawal benefit of 5% dollar to dollar. LifeGuard Freedom Flex income rider is a lifetime (GMWB) guaranteed minimum withdrawal benefit based on an age besed schedule. The percentage received is based on age at first withdrawal, but the guaranteed annual withdrawal amount (GAWA) may increase upon a step-up. The Jackson non-commissionable fee-only Jackson Advisory Perspective II has these same income riders available.

The Agent sales pitch for this annuity?

These retirement annuities, also called an hybrid annuity, will likely be presented on three ideas:

1. Market explosure with upside potential from investment choices

2. Lifetime Income features & Death Benefits

3. Potential bonus money

The Jackson Perspective II annuity is for retirement investors that want options to customize there needs like a swiss army knife for investments. With double digit optional riders for income and death benefit no wonder this is the best selling variable annuity on the market for years. Some of the income riders have several choices of upfront bonuses to the income account from 5% up to 7%. The higher the bonus the more costly the annual income rider fee is.

Over the long term, this annuity will generate market like returns minus the 1.3% admin cost and the optional riders of 1% plus annual fee.

Annuities provide an attractive and simple way to plan for retirement, With the help of optional features, such as riders and accounts that provide additional benefits based on what best suits your need at any given time during retirement planning. These products can be used in conjunction with other investments like bonds or fixed-income assets while still offering the benefits of long-term financial stability that comes from investing in one investment option only.