What Will We Cover in this Annuity Review?

In this annuity review, we will be going over annuity details regarding the Brighthouse Shield Level annuity.

- Investment type

- Return expectations

- Optional Riders

- Fees

- Rates

Servicing the retirement income planning market has grown in popularity as baby boomers and retirees search for options to protect against market volatility and secure lifetime income. Annuities are one of the few strategies that can accomplish both secured growth and guaranteed income.

Investors like you doing research on annuities to combat the above concerns are finding it more difficult with all the different types of annuities like “hybrid” annuities, equity-linked annuities, buffer annuities, fixed index annuities (FIA), and variable annuities. The best selling retirement annuity of 2021 is the registered index-linked annuity (RILA), the $17.4 billion market for structured variable annuities– also sometimes referred to as a variable indexed annuity, structured variable annuity, buffer annuity, or a structured annuity – is essentially a blend of the best part of a variable annuity and limited downside protection of a fixed indexed annuity (FIA).

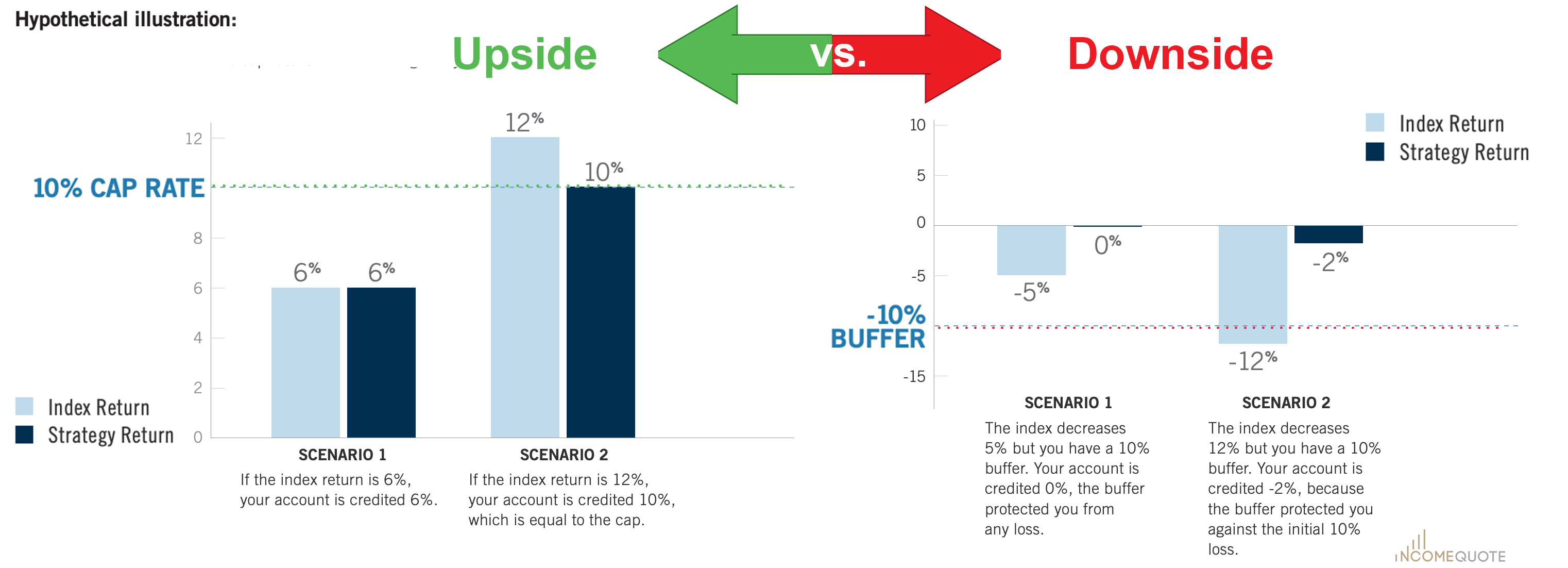

Started in 2010 with one company, these hybrid annuities do offer is a “limited loss” to an investor – between 10% and 20% of the market’s decline during a specified period usually a year period. For example, if a RILA or buffer annuity has selected the optional 20% S&P 500 index protection against a market loss over one year period, an investor’s account would lose only 8% of its value if the market dropped by 28% in that given year because of the buffer annuity protects the first 20% loss from the market.

The more loss protection or buffer you select, the less upside gain from the index you will receive.

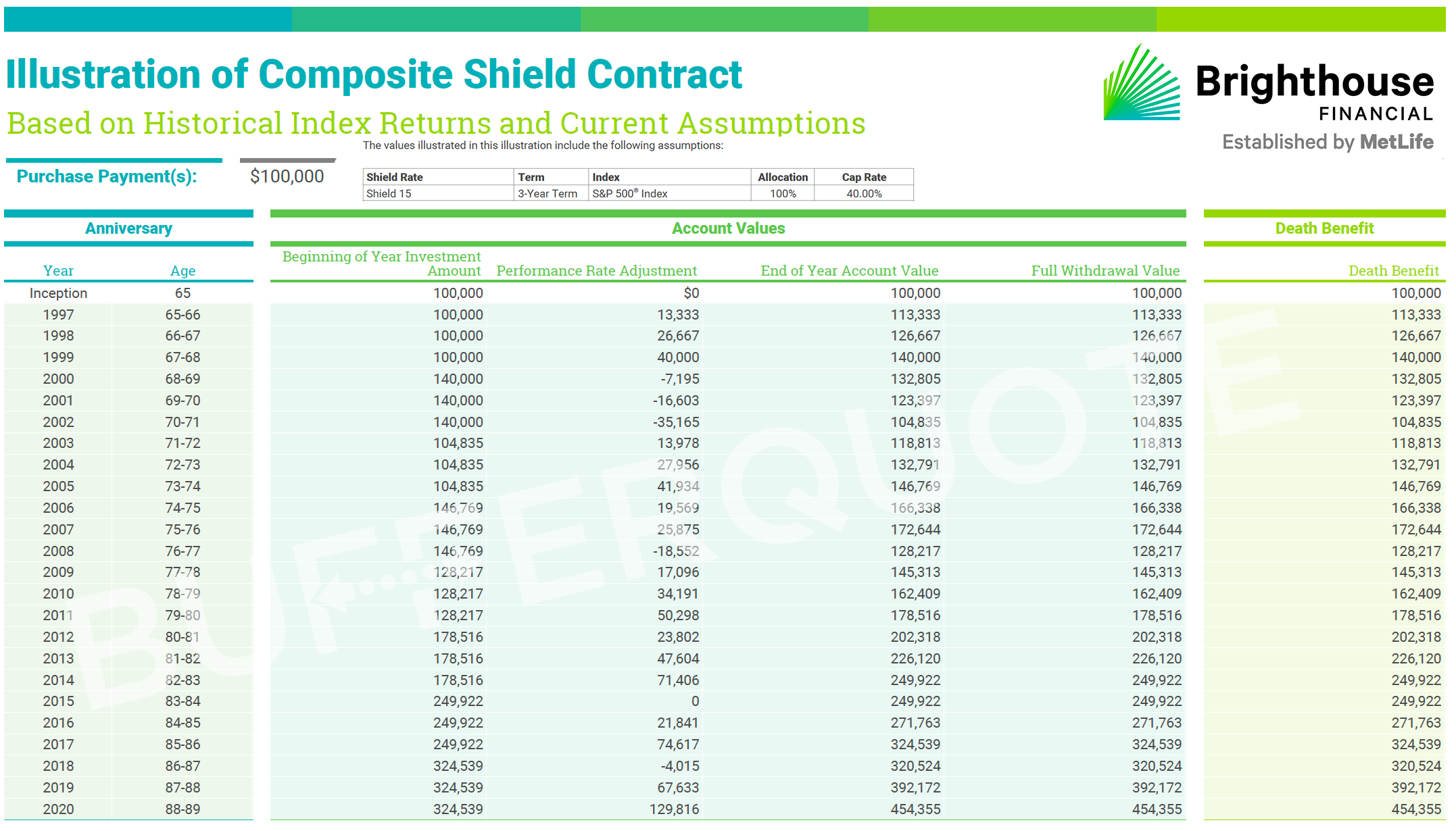

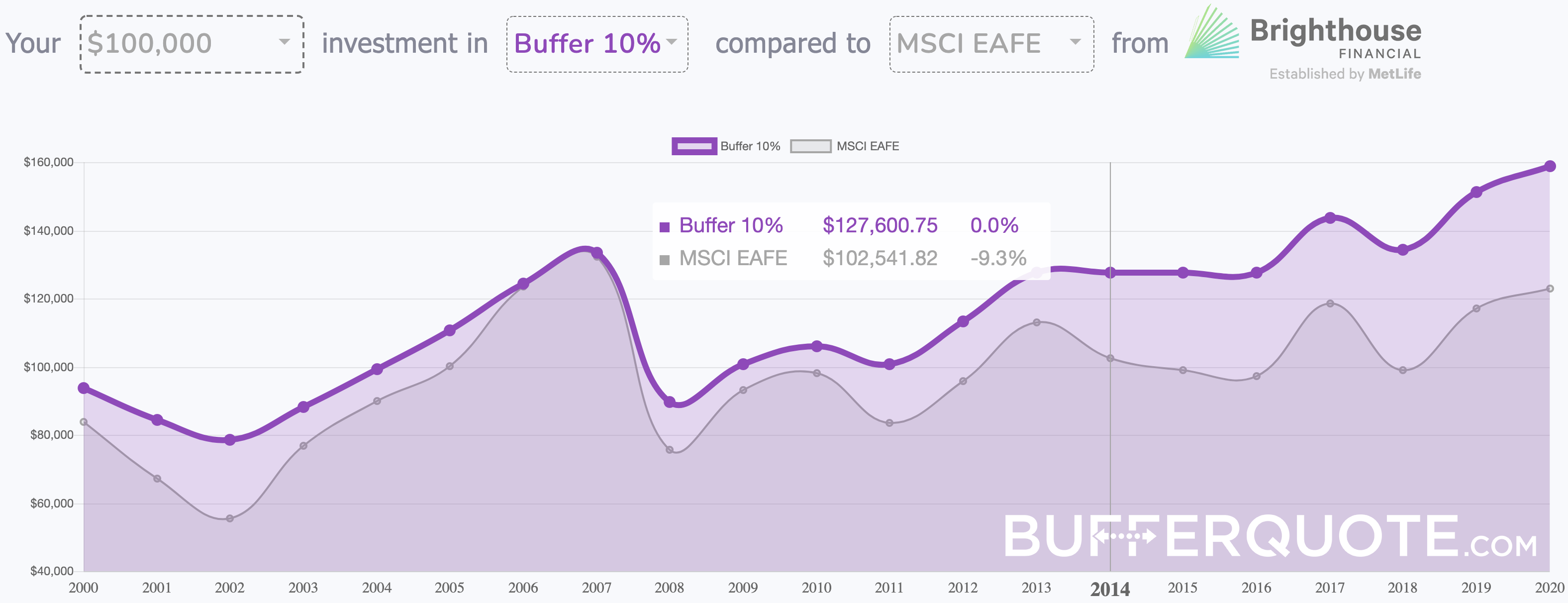

Taken from the interactive chart above the buffer annuity invested in the International MSCI EAFE index over the last 20 years gain more than $36,000 than the MSCI EAFE index. That was an increase of 20% gain from limiting market losses with the 10% market protection each year. Click the chart to see how it works.

Annuity Company Issuer Review: Brighthouse Financial

Since this investment is usually for the long term such as 10 years, it is important that the annuity company itself is financially sound. The guarantees in the annuity are back by the insurance company and not from a government agency. However each state’s Guaranty Association has a dollar amount, usually $100,000, that it will refund if an annuity carrier went bankrupt. Think of it as a second layer of protection.

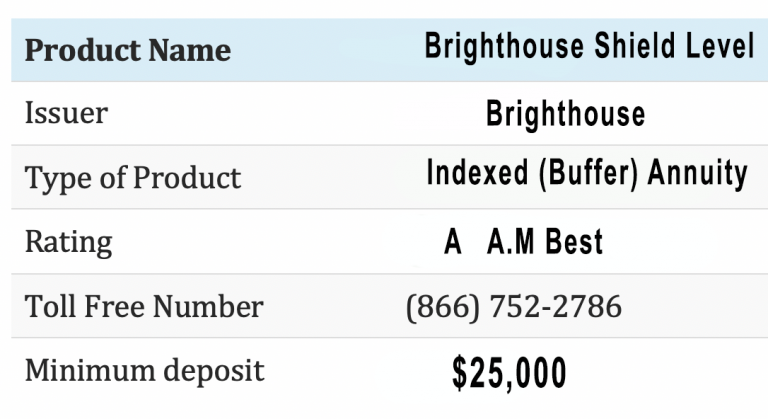

Brighthouse Financial, Inc. is one of the largest providers in America with $219 billion dollars worth or assets and approximately 2 million insurance policies annuity contracts currently under force nationwide alone! On August 4th 2017 after being separated from MetLife for over 6 decades this company began trading on Nasdaq stock market under BHF symbol where they retain a 19% stake belonging only to themselves while also becoming more popular than ever before due to its large scope which has helped increase revenue stream by almost 10%. Headquartered in Charlotte, North Carolina, the company began selling annuity and life insurance under the Brighthouse Financial brand on March 6, 2017.

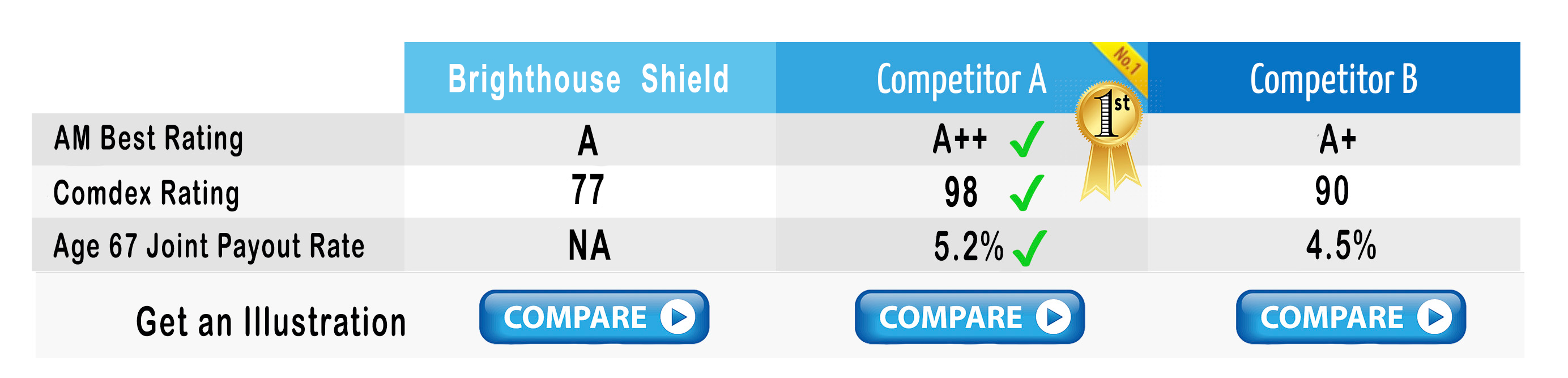

Brighthouse Financial has an A.M Best rating as of February 2022 of A and a Comdex rating of 77.

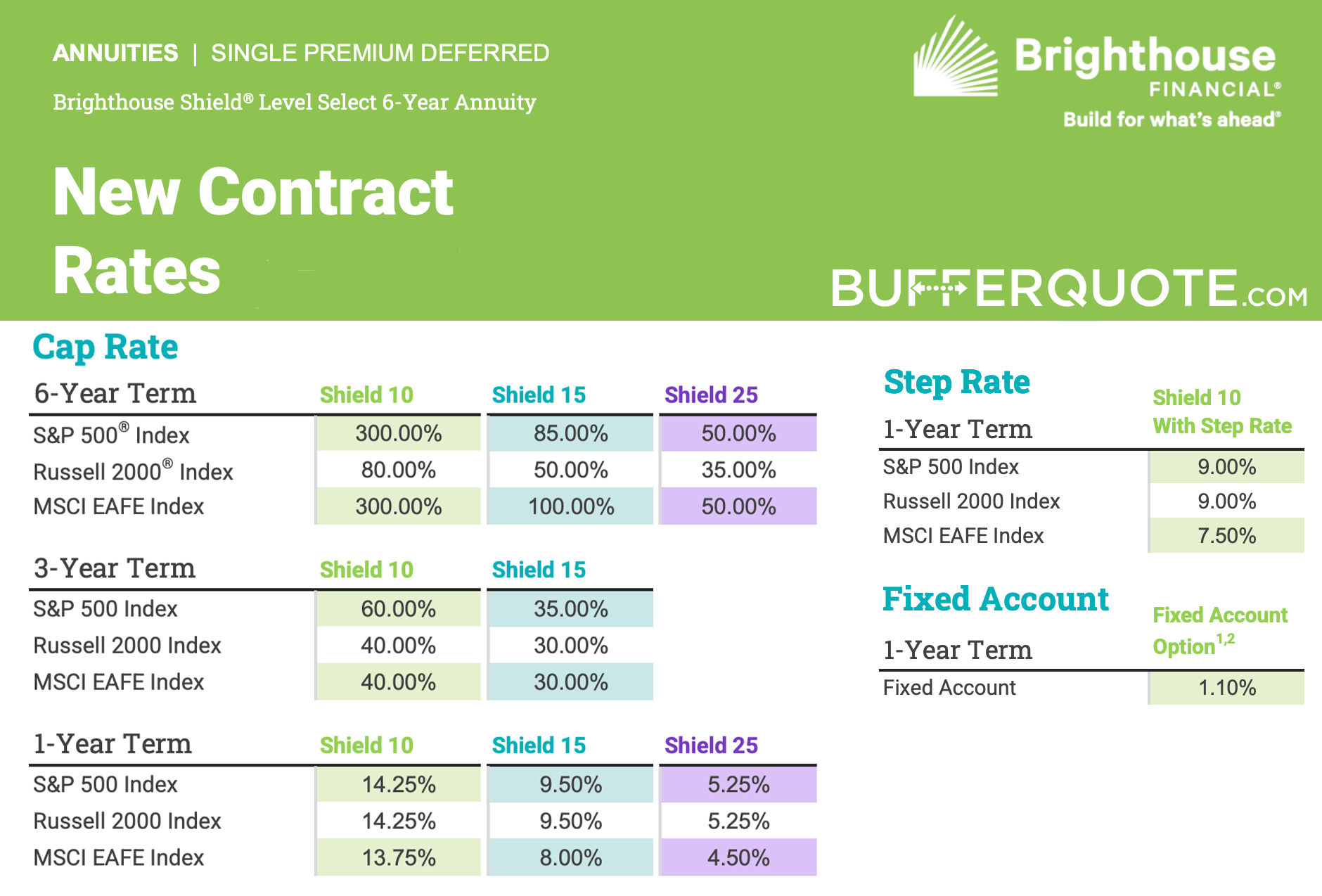

Earning Interest:

Shield Annuity is a customizable indexed variable annuity that allows you to make choices based on your individual retirement needs and change themes those needs evolve.

One of the most valuable aspects of Shield Level annuity is its potential to cushion your account against loss. With Brighthouse Shield annuity, you can select a level of protection, called a buffer, which may help limit loss in down markets, partially shielding your account in the case of a negative index return.

With the help of the buffer, your risk of loss could be lessened. You also have the opportunity to grow your money in up markets by choosing from index strategies.

When it comes to choosing an annuity, there are a lot of factors that you need consider. One thing in particular is your tolerance for risk and what kind would be most appropriate depending on this can depend largely on the type either fixed indexed or variable but some people might want both low downside exposure with limited market volatility as well as high growth potential which could make them interested specifically looking at Buffer annuity options.

Fixed indexed annuities and RILAs provide the opportunity for growth based on performance of stock market index. Other similarities include tax-deferred potential, annual free withdrawal amounts as well an option convert into stream income payments in retirement. Both fixed indexed annuity nor rila directly participate equity investments but differ from one another by accepting higher risk with greater upside possibilities.

How it works

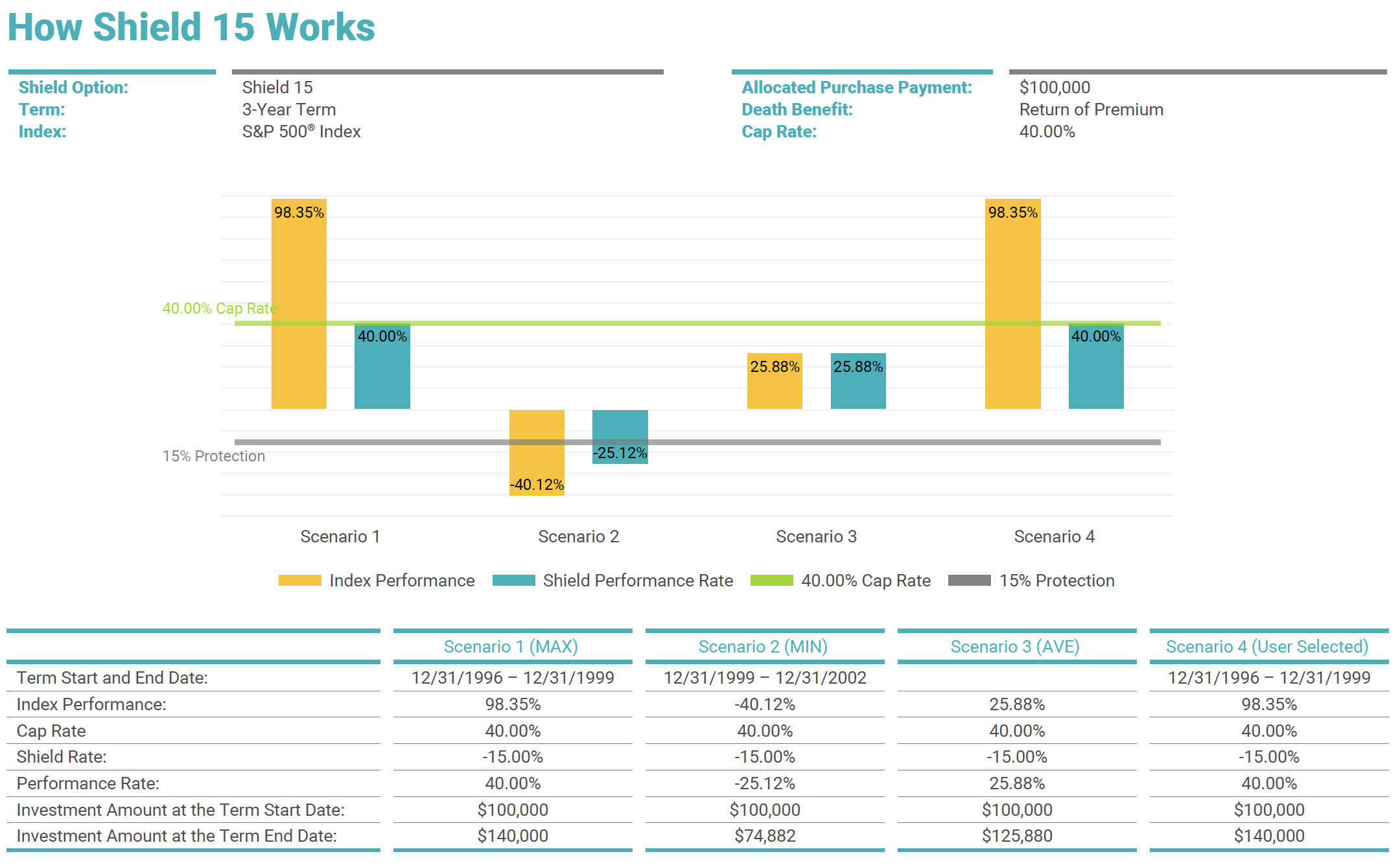

The upside and downside limits of RILAs are connected, so a higher level of protection from downside risk means a lower cap on upside potential, and vice versa. When index performance is positive during a term, your annuity may earn interest credits, limited by a cap or participation rate. Index declines can result in negative interest credits, with a level of protection from any loss.

Downside protection

A “buffer” and a “floor” are two options that limit exposure to market loss.

Buffer: Percentage of downside protection, typically 10, 15 or 20 percent. For example, if an index declines 15 percent and you choose a 10 percent buffer, you would incur a loss of 5 percent.

Floor: Opposite of the buffer option. In this case, you would be exposed to the percentage loss up to the floor amount, but you are protected against any loss after this percentage. For example, if you choose a product with a 10 percent “floor” and the market declines 15 percent, you would lose 10 percent, because the floor limits the downside

Shield Level also enables you to diversify where you put your money by allocating across well-known indices. S&P 500, MSCI EAFE, EURO STOXX 50®, iSHARES RUSSELL 2000 ETF, and Nasdaq 100. Because different indices perform differently under similar market conditions, diversification can help improve your opportunity for growth.