What Will We Cover in this Annuity Review?

In this annuity review we will be going over annuity details regarding the Allianz Index Advantage

Variable annuity.

- Investment type

- Rates

- Optional Riders

- Fees

- Return expectations

Servicing the retirement income planning market has grown in popularity as baby boomers and retirees search for options to protect against market volatility and secure lifetime income. Annuities are one of the few strategies that can accomplish both secured growth and guaranteed income.

Investors like you doing research on annuities to combat the above concerns are finding it more difficult with all the different types of annuities like “hybrid” annuities, equity-linked annuities, buffer annuities, fixed index annuities (FIA), and variable annuities. The best selling retirement annuity of 2021 is the registered index-linked annuity (RILA), the $17.4 billion market for structured variable annuities– also sometimes referred to as a variable indexed annuity, structured variable annuity, buffer annuity, or a structured annuity – is essentially a blend of the best part of a variable annuity and limited downside protection of a fixed indexed annuity (FIA).

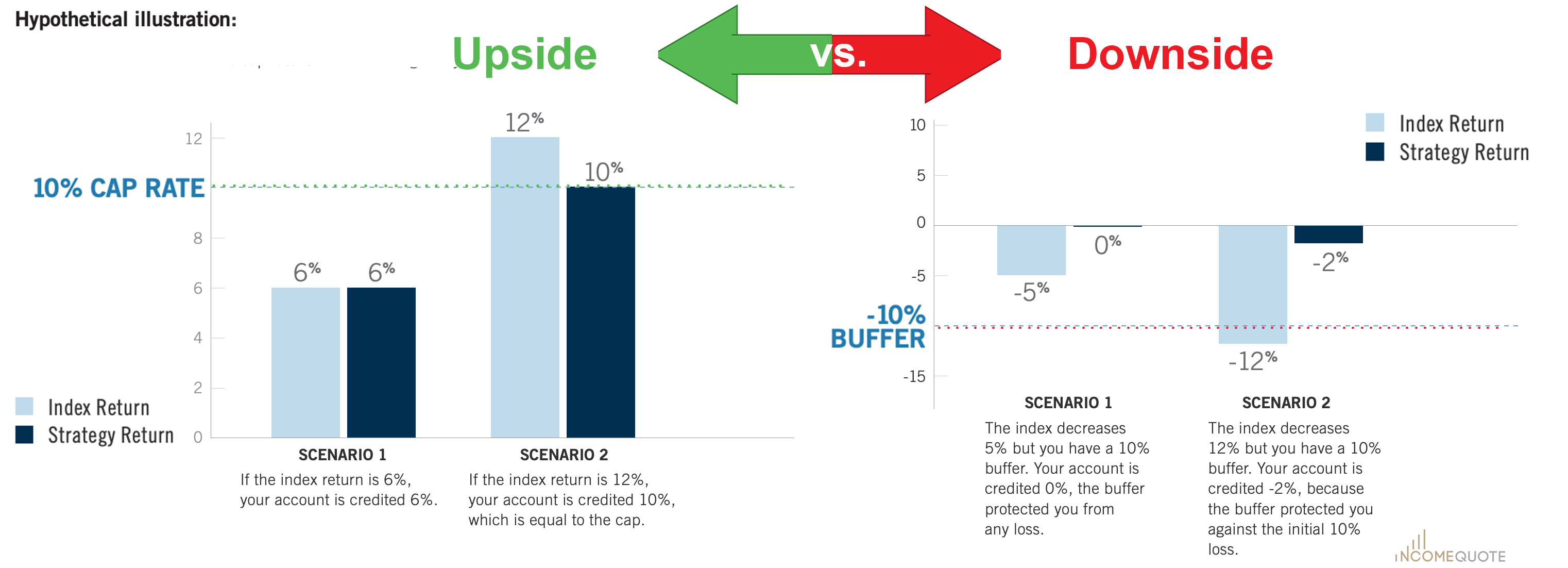

Started in 2010 with one company, these hybrid annuities do offer is a “limited loss” to an investor – between 10% and 20% of the market’s decline during a specified period usually a year period. For example, if a RILA or buffer annuity has selected the optional 20% S&P 500 index protection against a market loss over one year period, an investor’s account would lose only 8% of its value if the market dropped by 28% in that given year because of the buffer annuity protects the first 20% loss from the market.

The more loss protection or buffer you select, the less upside gain from the index you will receive.

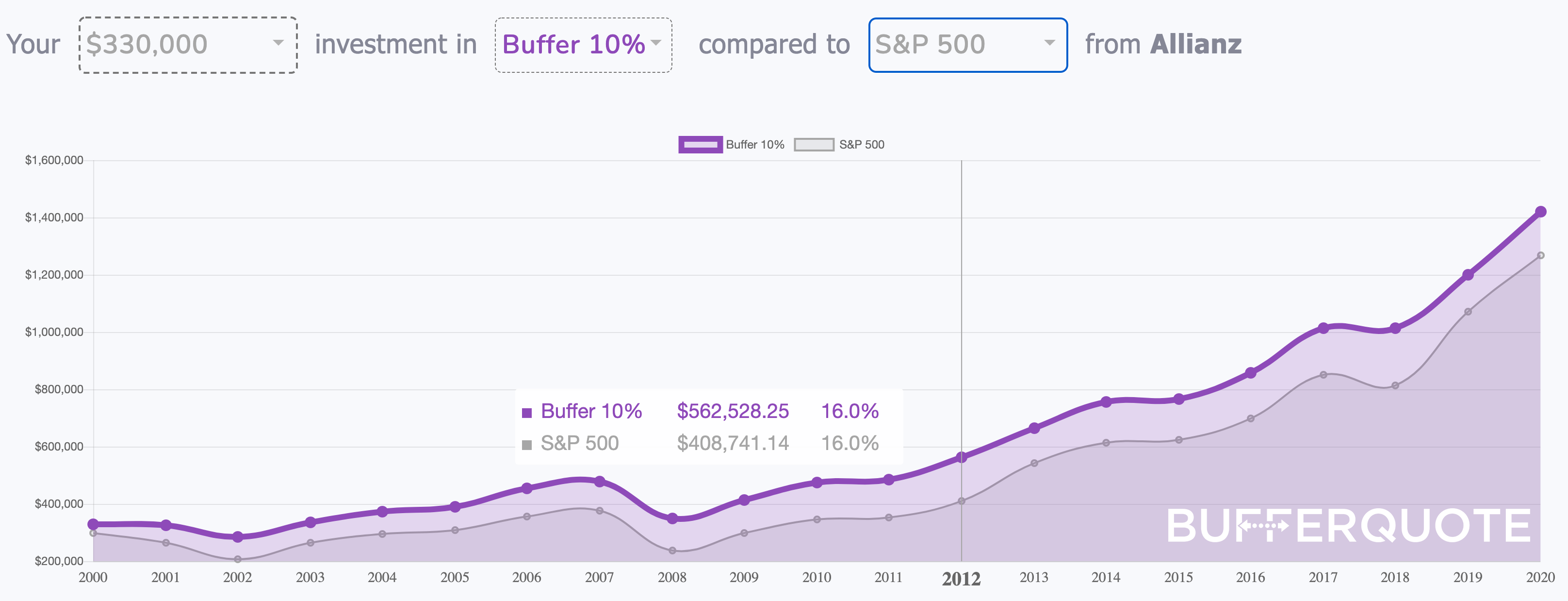

Taken from the interactive chart above the buffer annuity invested in the S&P 500 index over the last 20 years gain more than $86,000 than the S&P 500 index. That was an increase of 45% gain from limiting market losses with the 20% market protection each year. Click the chart to see how it works.

Annuity Company Issuer Review: Allianz

Since this investment is usually for the long term such as 10 years, it is important that the annuity company itself is financially sound. The guarantees in the annuity are back by the insurance company and not from a government agency. However each state’s Guaranty Association has a dollar amount, usually $100,000, that it will refund if an annuity carrier went bankrupt. Think of it as a second layer of protection.

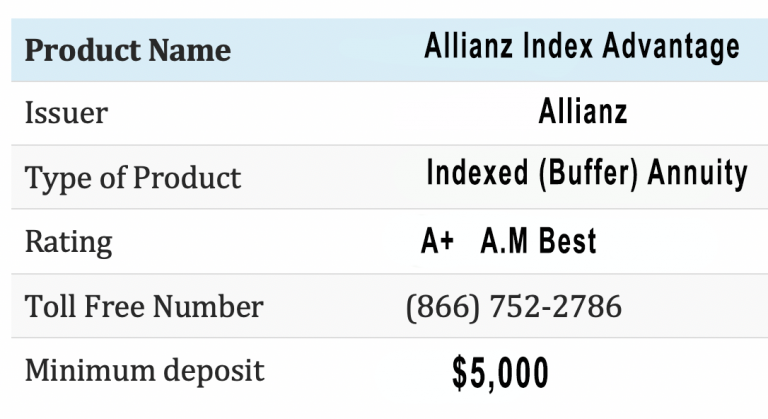

Sometimes their misspelled name as Alliance, but Allianz Life Insurance Company of North America has been keeping its promises since 1896. Today, it carries on that tradition, helping Americans achieve their retirement income goals with a variety of annuities and life insurance products. As a leading provider of fixed annuities, Allianz Life is part of Allianz SE, a global leader in the financial services industry with nearly 155,000 employees worldwide. Based on its revenue, Allianz SE is the 20th largest company in the world (Fortune Global 500, August 2010).

Sometimes their misspelled name as Alliance, but Allianz Life Insurance Company of North America has been keeping its promises since 1896. Today, it carries on that tradition, helping Americans achieve their retirement income goals with a variety of annuities and life insurance products. As a leading provider of fixed annuities, Allianz Life is part of Allianz SE, a global leader in the financial services industry with nearly 155,000 employees worldwide. Based on its revenue, Allianz SE is the 20th largest company in the world (Fortune Global 500, August 2010).

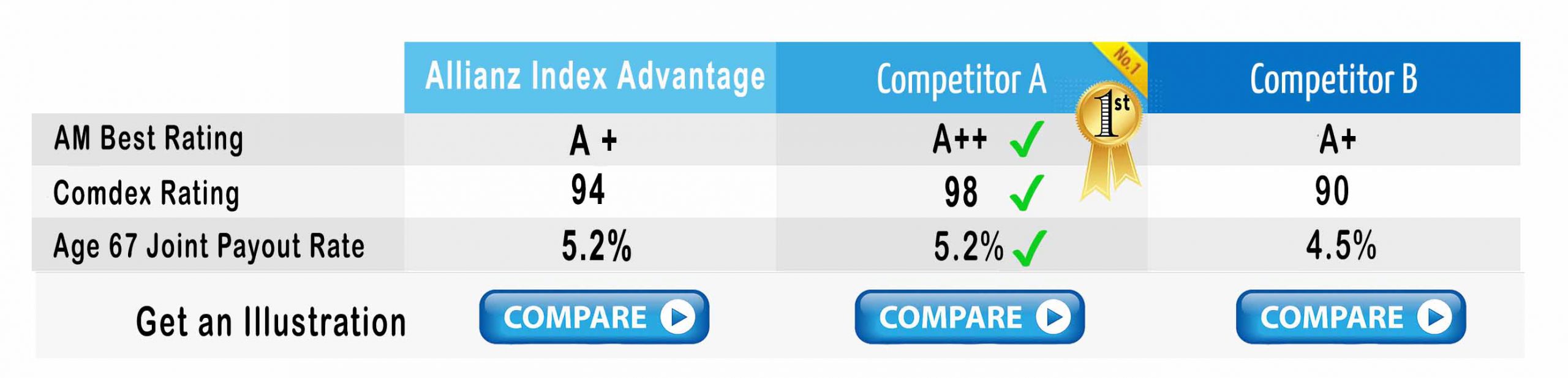

Allianz has an A.M Best rating as of April 2021 of A+ and a Comdex rating of 94.

Earning Interest:

Index Advantage is a customizable indexed variable annuity that allows you to make choices based on your individual retirement needs and change themes those needs evolve.

One of the most valuable aspects of Indexed Advantage is its potential to cushion your account against loss. With Allianz Index Advantage index strategies, you can select a level of protection, called a buffer, which may help limit loss in down markets, partially shielding your account in the case of a negative index return.

With the help of the buffer, your risk of loss could be lessened. You also have the opportunity to grow your money in up markets by choosing from index strategies.

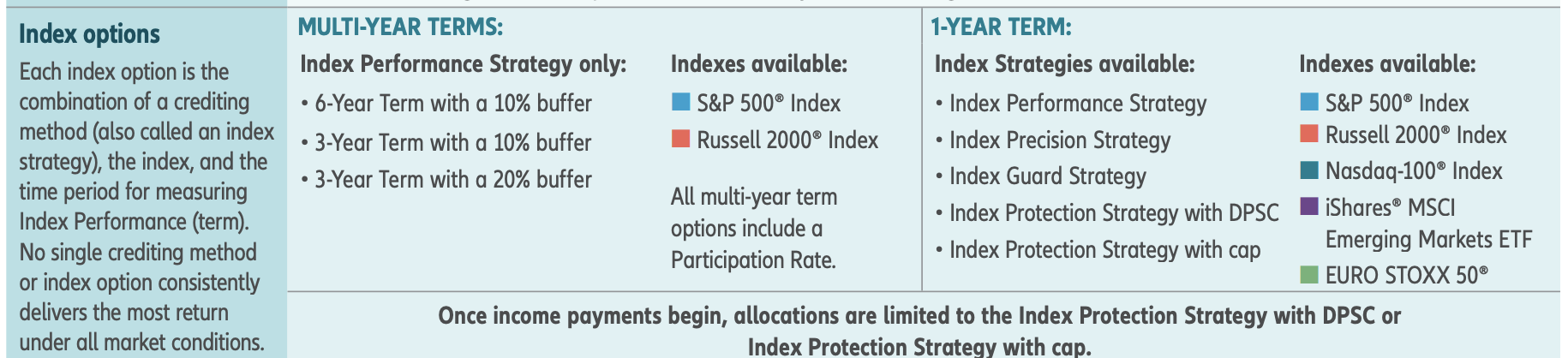

1-YEAR TERM STRATEGIES:

Index Performance Strategy

- Provides greater performance potential, based on a cap, among 1-year term strategies

- Provides a level of protection with a buffer that absorbs the first 10% of negative index performance

- This strategy may perform best in a strong market with protection from smaller index losses

Index Precision Strategy

- Offers the same level of protection and 10% buffer as the Index Performance Strategy

- Credits an annual predetermined Precision Rate if the change in the annual index value is zero or positive

- This strategy may perform best in a low growth environment with protection from smaller index losses

Index Guard Strategy

- Offers upside potential that may be matched or exceeded only by the Index Performance Strategy

- Provides a level of protection with a 10% floor which means you assume the first 10% negative index loss and no more

- This strategy may perform best in a strong market with protection from large index losses

Index Protection Strategy with cap and Index Protection Strategy with Declared Protection Strategy Credit (DPSC)

- These provide the most protection with no losses due to negative market index returns

- Offers modest growth potential with a DPSC relative to the other strategies

Once income payments begin, allocations are limited to the Index Protection Strategy with DPSC or cap.

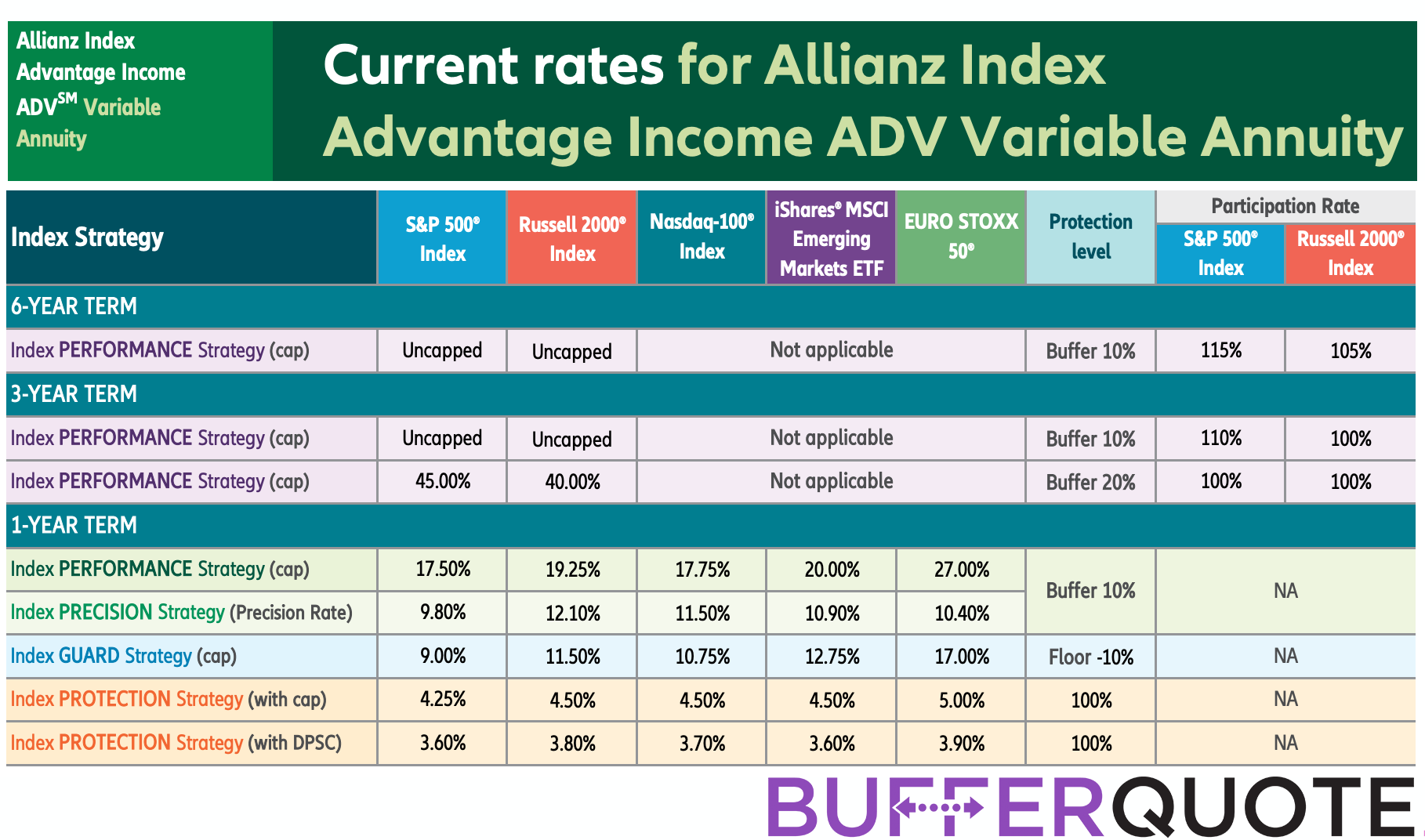

Each index strategy determines how your money can grow and calculates the interest you can earn differently.

Index Advantage also enables you to diversify where you put your money by allocating across well-known indices. S&P 500, MSCI EAFE, EURO STOXX 50®, iSHARES RUSSELL 2000 ETF, and Nasdaq 100. Because different indices perform differently under similar market conditions, diversification can help improve your opportunity for growth.

How to use this annuity for retirement?

Fixed annuities provide an attractive and simple way to plan for retirement, With the help of optional features, such as riders and accounts that provide additional benefits based on what best suits your need at any given time during retirement planning. These products can be used in conjunction with other investments like bonds or fixed-income assets while still offering the benefits of long-term financial stability that comes from investing in one investment option only.

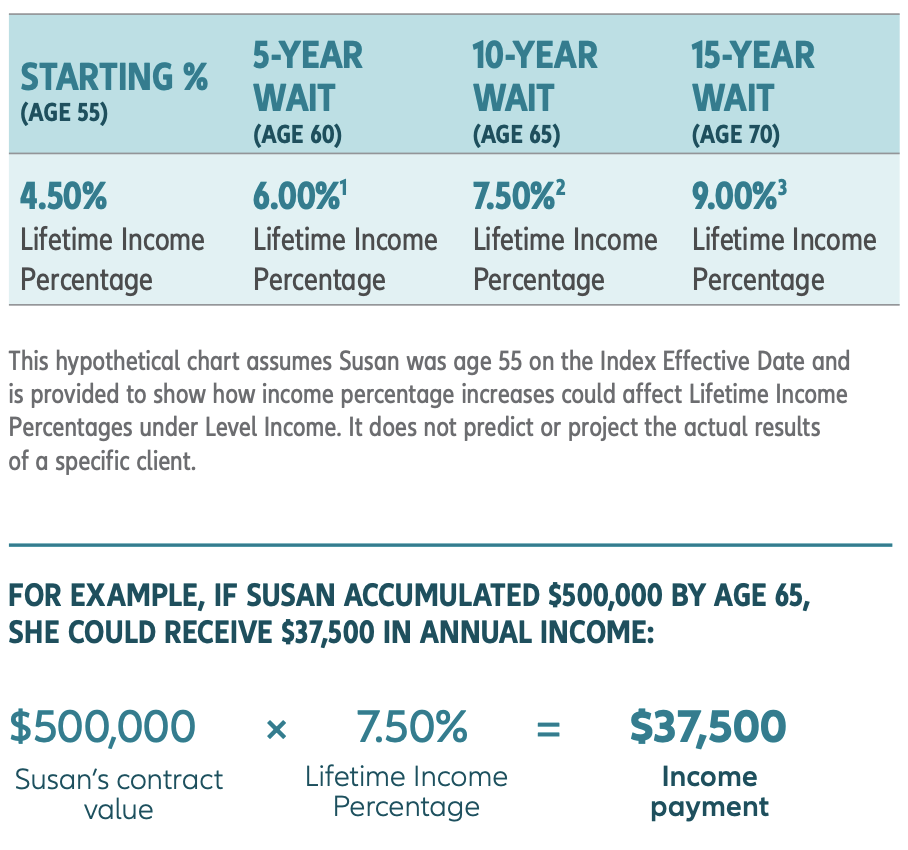

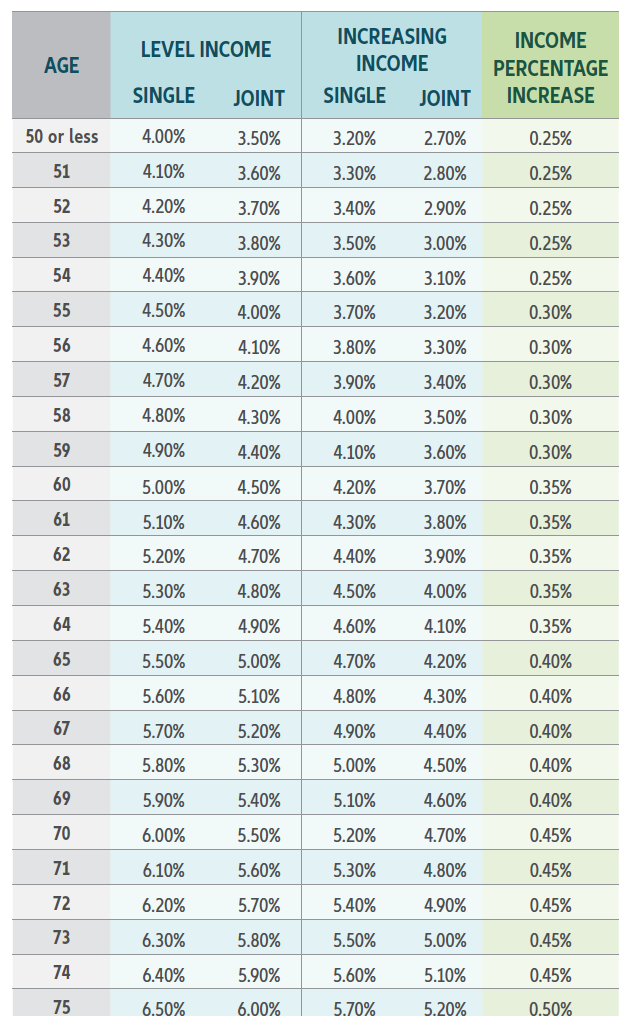

Index Advantage Income ADV can help you safely secure your retirement even if the markets are unstable. With Index Advantage Income ADV, your Lifetime Income Percentage has the opportunity to increase each year, even if your retirement assets fluctuate.  Beginning at age 45, the annuity provides a guaranteed income percentage increase in each of your Lifetime Income Percentages for each year you wait before beginning income payments. Index Advantage Income ADV is a great way to get your rewards when you’re patient. This chart compares options for Level Income and Increasing Income. It shows the income percentages and the annual income percentage. increases to those percentages based on the payment option and the age on the Index Effective date.

Beginning at age 45, the annuity provides a guaranteed income percentage increase in each of your Lifetime Income Percentages for each year you wait before beginning income payments. Index Advantage Income ADV is a great way to get your rewards when you’re patient. This chart compares options for Level Income and Increasing Income. It shows the income percentages and the annual income percentage. increases to those percentages based on the payment option and the age on the Index Effective date.

Allianz Index Advantage Income ADV Variable Annuity with a single purchase payment and does not take any withdrawals prior to retirement. Reassurance of level and dependable income for life, Level Income

payments are selected. Not knowing when to receive income payments, available Lifetime Income Percentages can increase by 0.30% for every year you wait with Indexed Advantage Income annuity.