How this Annuity Review “Look” will help you.

Annuities have become a hot topic in today’s financial world for several reason.

- Stock Market volatility with downturns in the 30% range have crushed retirees portfolios that don’t have enough time to recover

- 10,000 Baby Boomers a day retire and look to secure a monthly income check from their “nest egg” portfolios.

Investors like you doing research on annuities to combat the above concerns are finding it more difficult with all the different types of annuities like “hybrid” annuities, equity linked annuities, fixed index annuities and variable annuities. More moving parts in these annuities make it hard to get to the end game simple solutions of “Will this investment help me in retirement?”. As a CFP®, Certified Financial Planner, I am a Independent Fiduciary and have to do what is best for you. Let’s get started.

What Will We Cover in this Annuity Review?

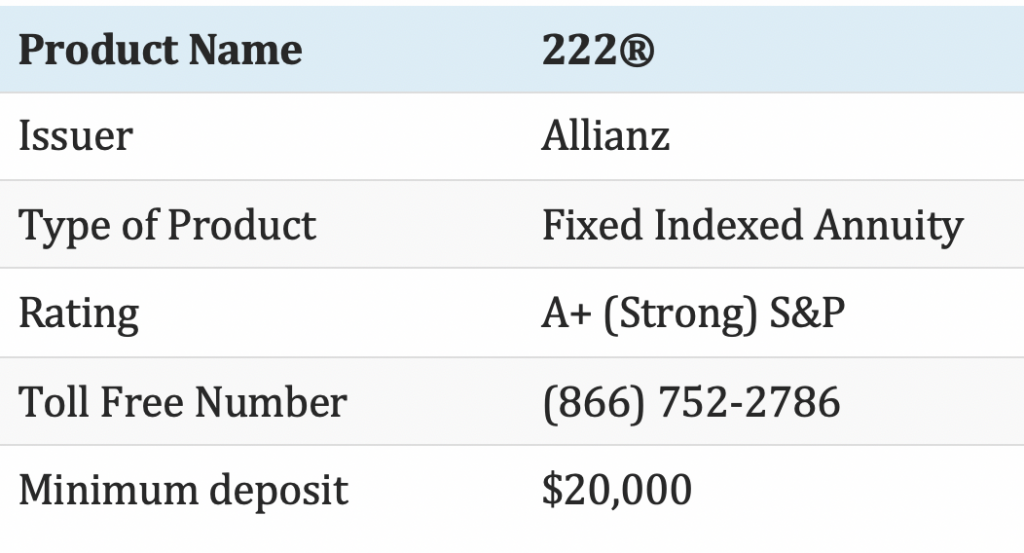

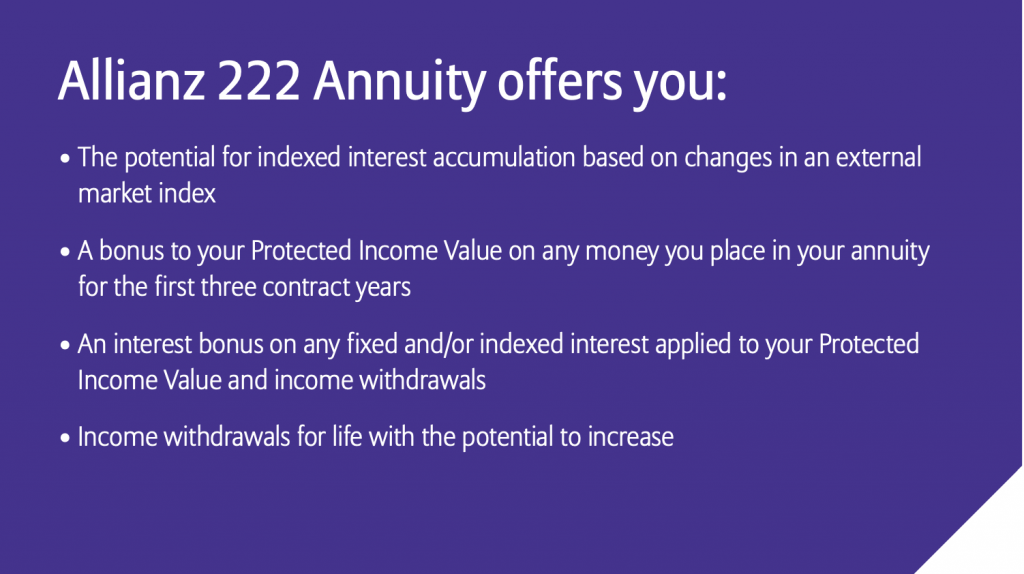

In the last handful of years annuities have become more integrated in the financial plan of future retirees. Annuities now have powerful optional features that focus on income riders, extended home healthcare income enhancements, enhanced death benefits and different confusing interest crediting methods. Famously marketed as “hybrid annuities” which combine various optional features of other annuity types. Sadly, there’s a lot of misinformation about how they really work and should be used in your financial plan. In this annuity “Look”, we will be going over annuity details regarding the Allianz 222 fixed indexed annuity, regarding:

- Investment type

- Rates

- Optional Riders

- Fees

- Return expectations

- How it is used- Pros and Cons

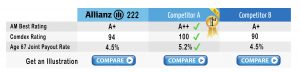

Comparison:

Table below will update as the competition changes. Currently, there are some competitors to the Allianz 222 index annuity. To request a side by side, click on the compare button below and our Certified Financial Planner® will be happy to answer any question you might have.

Servicing the retirement income planning market has grown in popularity as baby boomers and retirees search for options to protect against market volatility and secure lifetime income. Annuities are one of the few strategies that can accomplish both secured growth and guaranteed income. According to Life insurance industry group LIMRA, in 2018 over $132 billion in fixed annuity annual sales occurred. With Fixed Indexed annuities sales projected to grow nearly forty percent by the year 2023. A turbulent stock market encourages investors to seek less risky havens for their money, such as fixed annuities, said Todd Giesing, director of annuity research at LIMRA.

Annuities come in different specialties and many annuity carriers have different products within the same categories such as three different fixed index annuities. Each having a different focus such as secured growth or death benefits as examples. Along with different available riders or options attached to your annuity, one annuity product could be completely different from your neighbor with the same named annuity but without certain riders attached.

Annuity Company Issuer Review: Allianz SE and Allianz Life

Since this investment is usually for the long term such as 10 years, it is important that the annuity company itself is financially sound. The guarantees in the annuity are back by the insurance company and not from a government agency. However each state’s Guaranty Association has a dollar amount, usually $100,000, that it will refund if an annuity carrier went bankrupt. Think of it as a second layer of protection.

Sometimes their misspelled annuity as Alliance 222 annuity, Allianz Life Insurance Company of North America has been keeping its promises since 1896. Today, it carries on that tradition, helping Americans achieve their retirement income goals with a variety of annuities and life insurance products. As a leading provider of fixed index annuities, Allianz Life is part of Allianz SE, a global leader in the financial services industry with nearly 155,000 employees worldwide. Based on its revenue, Allianz SE is the 20th largest company in the world (Fortune Global 500, August 2010).

Allianz Life is part of Allianz SE, a global leader in the financial services industry with nearly 155,000 employees worldwide. Based on its revenue, Allianz SE is the 20th largest company in the world (Fortune Global 500, August 2010).

Surrender Fees:

Surrender charges/fees and periods for this annuity are the typical of most indexed annuities. Most fixed index annuities will have a 5 year, 7 year, 10 year, and 14 year surrender variation to choose from. Taking the longer surrender period will most likely give you a larger cap on indexes and a larger fixed rate option for index crediting. Typically fixed index annuities allow you to withdraw 10% of your accumulation value after the first year without surrender fees. However if you are under age 59 and a half, you are subject to a 10% IRS tax penalty as well as income taxes applied to the withdrawal.

Allianz 222® has only the 10 year surrender charge option as seen above.

Earning Interest:

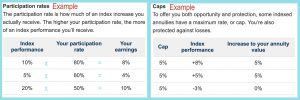

Indexed annuities do a lot of things to confuse investors. Too many moving parts when it should be a simple two part calculation. The two parts are index crediting and income crediting. See most index annuities have two values that are tracked each year. The accumulation value account or (walk away money) and income value account (Lifetime income calculation value).

The accumulation value account will be based on your chosen crediting method based on an index. Examples are Annual point-to-point or Participation rates. Each year this is calculated and showed on your annual annuity statement under names like annuity value or accumulation values.

The accumulation value account will be based on your chosen crediting method based on an index. Examples are Annual point-to-point or Participation rates. Each year this is calculated and showed on your annual annuity statement under names like annuity value or accumulation values.

The income value is usually calculated on some “bonus” or “roll up rate” each year with a maximum of ten years. This roll up rate can be simple interest or compound interest. Simple interest would be the same calculate interest every year ( 5% simple interest for 4 years at $100,000 deposit would equal $5,000 credit each year for 4 years). Compound interest would be calculated as follows ( 5% compound interest at $100,000 deposit would equal $5,000 credit first year, $5,250 year 2, and $5,512 year 3). Then the income value is multiplied by an age range percentage band to calculate your guaranteed lifetime income payment. Income values can also be called protected payment base or protected income value.

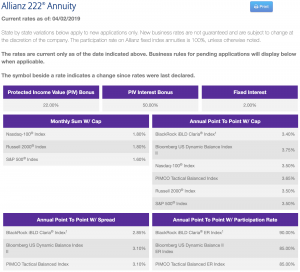

See current Allianz 222 rates here

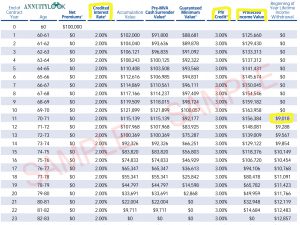

This is a sample Allianz 222 Illustration with the 100% in the fixed account giving it a 2% return only (conservative guarantee) in the Credited Interest Rate column, forth from left. This will give the PIV Credit column, eighth column from left, a 3% credit which is 50% of 2%. The PIV or Protected Income Value column then grows by 3% each year until income at year 10 is taken which is $9,018 and rising per year. Think of this as the worse case for guaranteed income unless your other crediting index like the S&P 500 gets a 0% credit in some years. So ask your agent for the 100% fixed option to show you what the income will be to compare to the highly credited run agent illustration. See if any other index annuities from different companies will beat that income amount. If you want to see if there are other annuities that can go up against the Allianz 222, contact us via the Free Annuity Help form.