What Will We Cover in this Annuity Review?

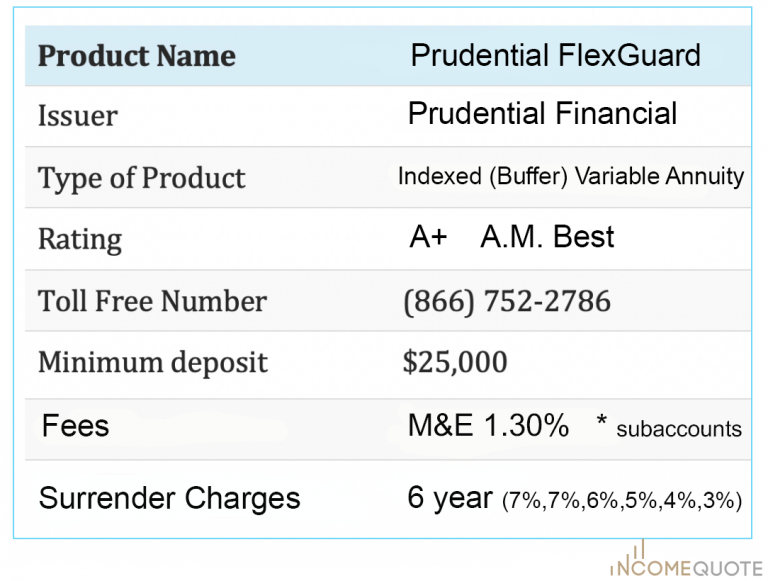

In this annuity review we will be going over annuity details regarding the Prudential Flex Guard Structed Variable annuity.

- Investment type

- Rates

- Optional Riders

- Fees

- Return expectations

Servicing the retirement income planning market has grown in popularity as baby boomers and retirees search for options to protect against market volatility and secure lifetime income. Annuities are one of the few strategies that can accomplish both secured growth and guaranteed income.

Investors like you doing research on annuities to combat the above concerns are finding it more difficult with all the different types of annuities like “hybrid” annuities, equity-linked annuities, buffer annuities, fixed index annuities (FIA), and variable annuities. The best selling retirement annuity of 2021 is the registered index-linked annuity (RILA), the $17.4 billion market for structured variable annuities– also sometimes referred to as a variable indexed annuity, structured variable annuity, buffer annuity, or a structured annuity – is essentially a blend of the best part of a variable annuity and limited downside protection of a fixed indexed annuity (FIA).

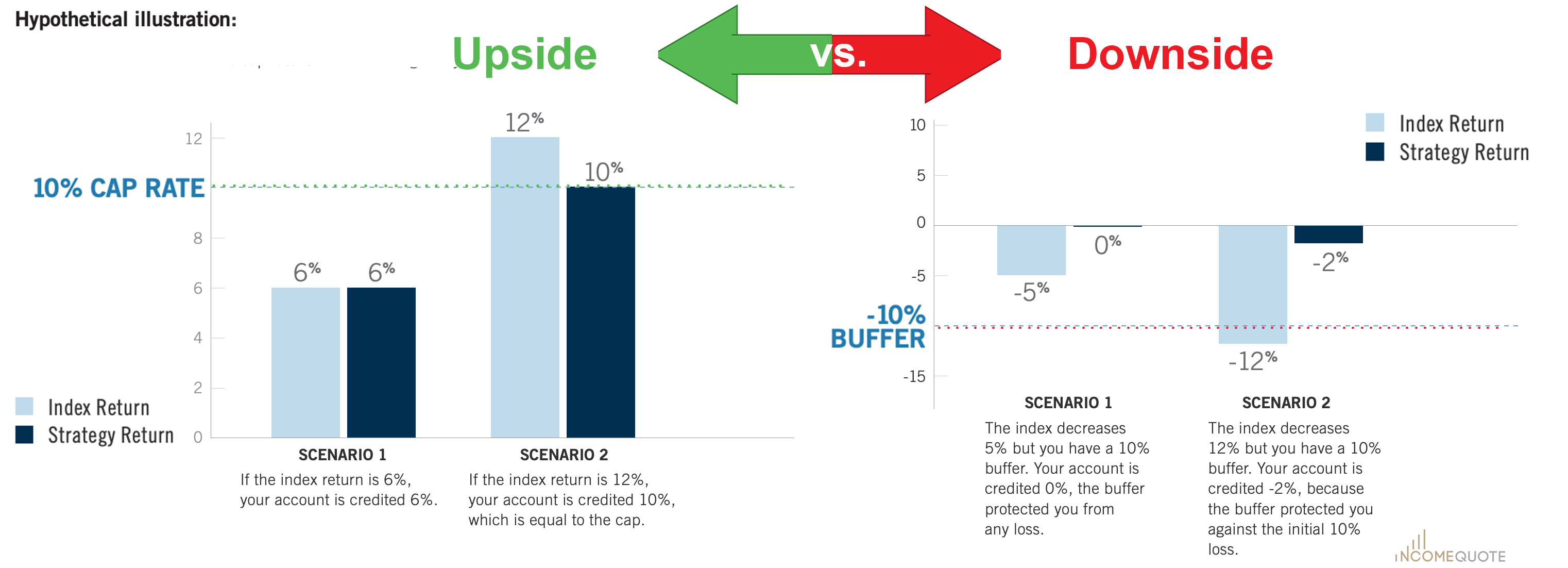

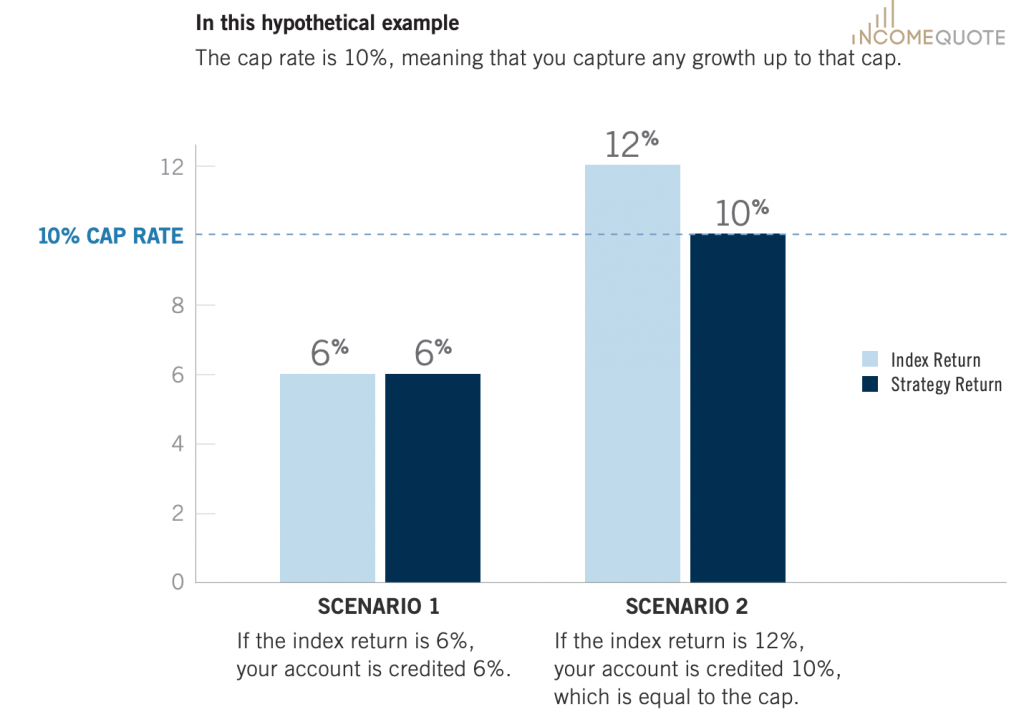

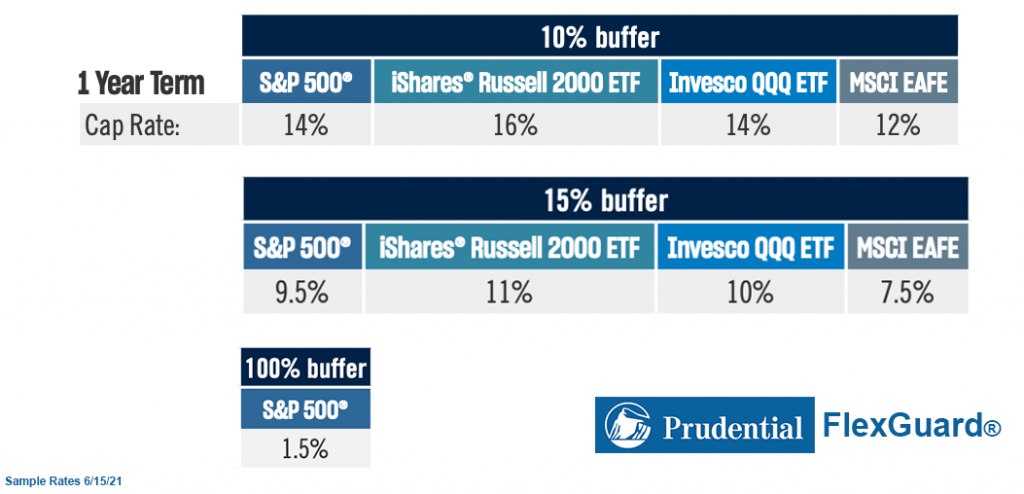

Started in 2010 with one company, these hybrid annuities do offer is a “limited loss” to an investor – between 10% and 20% of the market’s decline during a specified period usually a year period. For example, if a RILA or buffer annuity has selected the optional 20% S&P 500 index protection against a market loss over one year period, an investor’s account would lose only 8% of its value if the market dropped by 28% in that given year because of the buffer annuity protects the first 20% loss from the market.

The more loss protection or buffer you select, the less upside gain from the index you will receive.

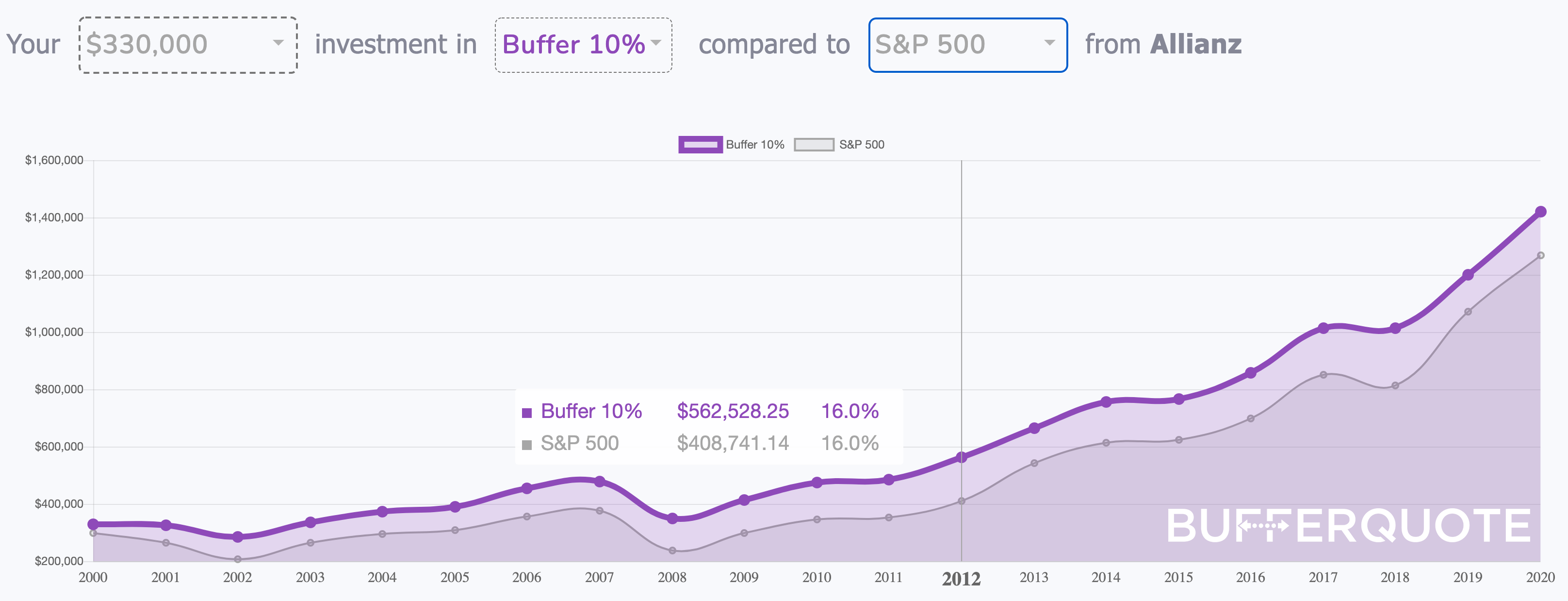

Taken from the interactive chart above the buffer annuity invested in the S&P 500 index over the last 20 years gain more than $86,000 than the S&P 500 index. That was an increase of 45% gain from limiting market losses with the 20% market protection each year. Click the chart to see how it works.

Annuity Company Issuer Review: Prudential Financial

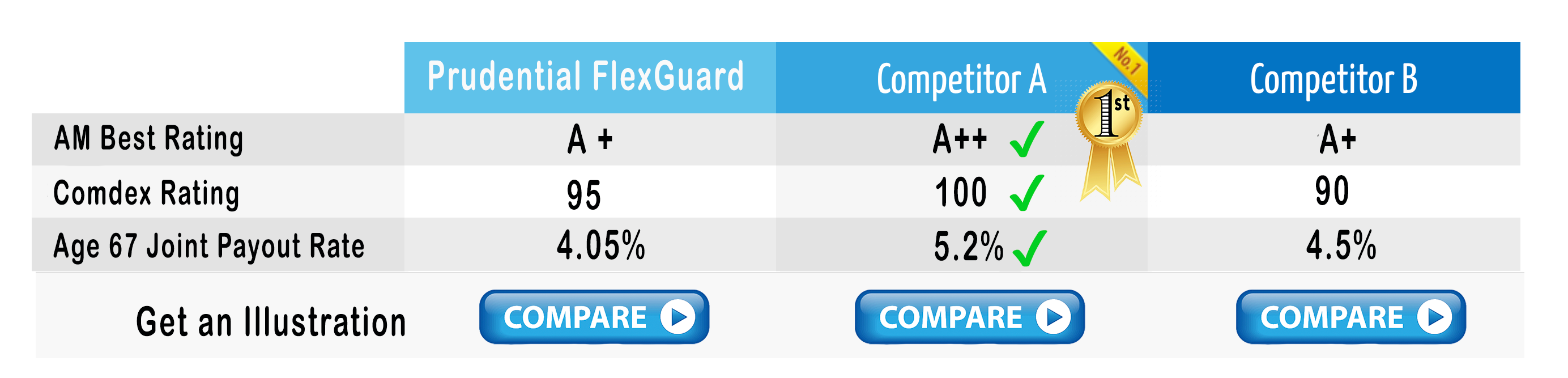

Prudential Financial, Inc. who’s symbol of the Rock of Gibraltar, has been keeping its promises since 1875. Prudential Financial, Inc. is an Fortune 500 and S&P 500 company whose subsidiaries provide insurance, investment management, and other retirement financial products to both retail and institutional customers. As of 2019, the Newark New Jersey company Prudential is the largest insurance provider in the United States with $815.1 billion in total assets. Prudential Financial was founded by soon to be US senator John Dryden in 1875 with it’s one product of burial insurance. Prudential’s A.M.Best rating is a A+ along with comdex score of 95.

Since this investment is usually for the long term such as 10 years, it is important that the annuity company itself is financially sound. The guarantees in the annuity are back by the insurance company and not from a government agency. However each state’s Guaranty Association has a dollar amount, usually $100,000, that it will refund if an annuity carrier went bankrupt. Think of it as a second layer of protection.