What is the hottest selling retirement annuity in 2021?

Annuities have become a hot topic in today’s financial world for several reasons.

- Stock Market volatility with downturns in the 30% range have crushed retirees portfolios that don’t have enough time to recover

- 10,000 Baby Boomers a day retire and look to secure a monthly income check from their “nest egg” portfolios.

Investors like you doing research on annuities to combat the above concerns are finding it more difficult with all the different types of annuities like “hybrid” annuities, equity-linked annuities, buffer annuities, fixed index annuities (FIA), and variable annuities. The best selling retirement annuity of 2021 is the registered index-linked annuity (RILA), the $17.4 billion market for structured variable annuities– also sometimes referred to as an indexed variable annuity, structured variable annuity, buffer annuity, or a structured annuity – is essentially a blend of the best part of a variable annuity and limited downside protection of a fixed indexed annuity (FIA).

Started in 2010 with one company, these hybrid annuities do offer is a “limited loss” to an investor – between 10% and 30% of the market’s decline during a specified period usually a year period. For example, if a RILA, indexed linked or buffer annuity has selected the optional 20% S&P 500 index protection against a market loss over one year period, an investor’s account would lose only 8% of its value if the market dropped by 28% in that given year because of the buffer annuity protects the first 20% loss from the market.

The more loss protection or buffer you select, the less upside gain from the index you will receive. Brighthouse Financial Shield Level annuity has a 12% gain limit yearly on the S&P 500 index with a 20% buffer protection on year loss.

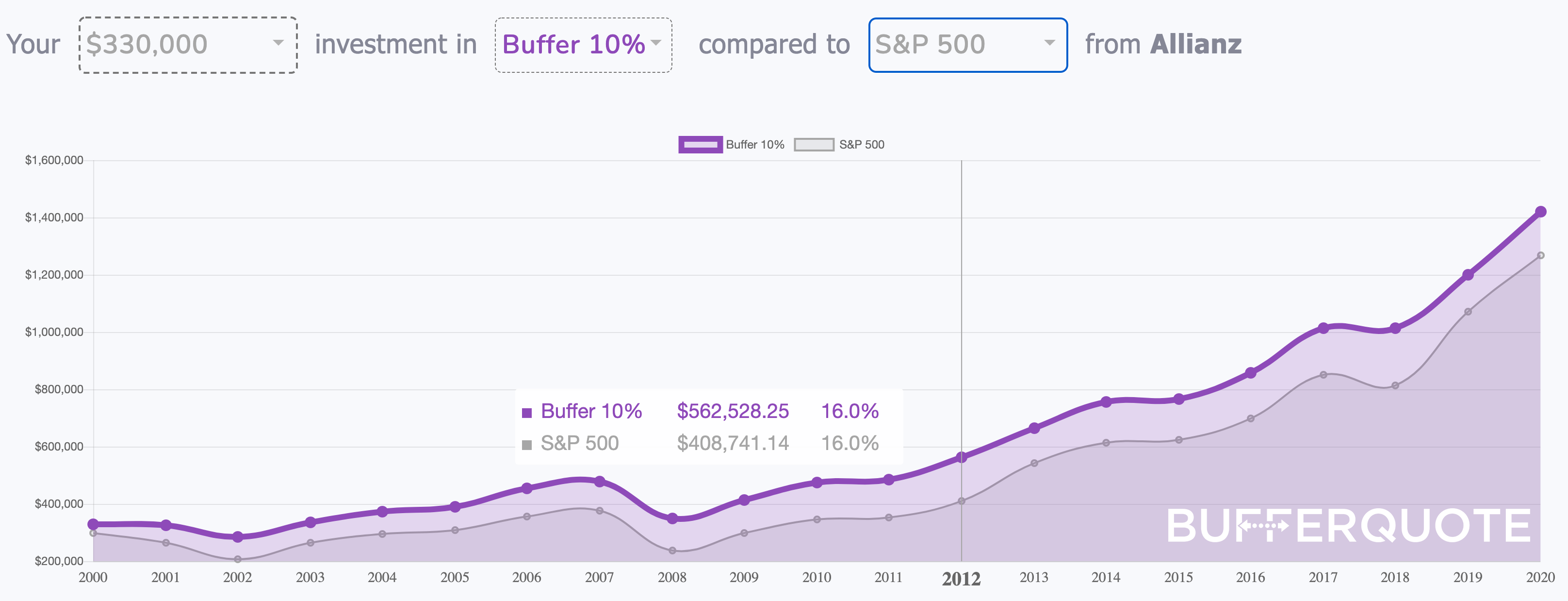

Taken from the interactive chart above the buffer annuity invested in the S&P 500 index over the last 20 years gain more than $86,000 than the S&P 500 index. That was an increase of 45% gain from limiting market losses with the 20% market protection each year. Click the chart to see how it works.

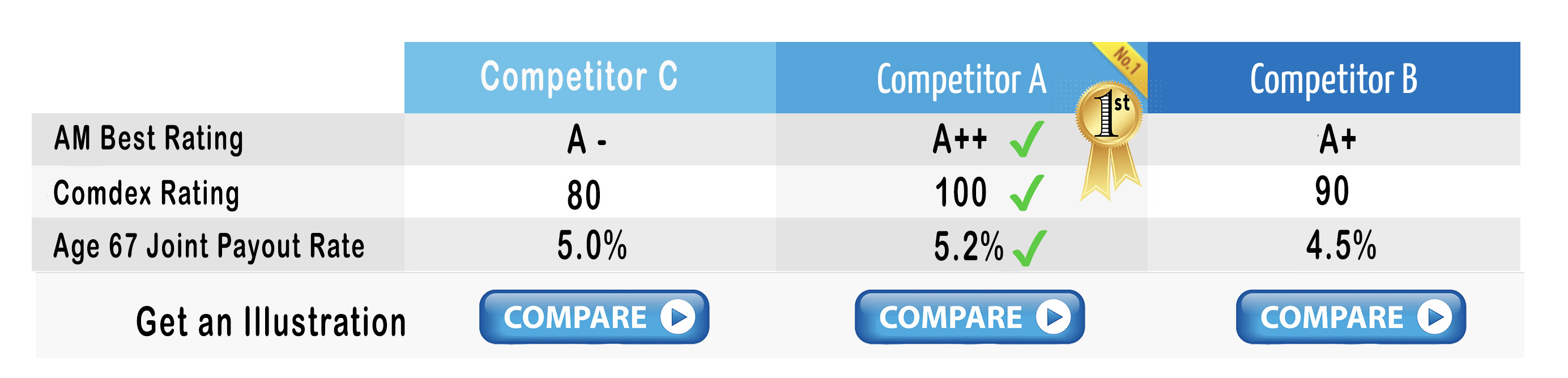

Only a small limited amount of annuity companies sell this product. However “The 100 Best Annuities for Today’s Market” annual article in Barron’s Magazine recognizes the index-linked variable annuity as one of the few best categories in the retirement planning tools. In addition to Brighthouse Financial’s Shield Level annuities, they are France-based AXA’s Equitable Structured Capital Strategies (SCS), Lincoln Financial’s Level Advantage annuity, Athene, and Allianz Index Advantage Variable annuity, and Prudential Flex Guard.